Central bank depository. Some policymakers take a hike.

SEI’s view

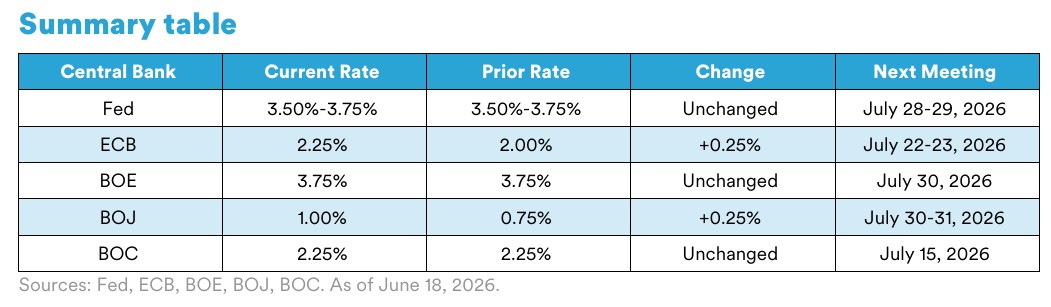

The Federal Reserve (Fed) held the federal funds rate steady for the fourth consecutive meeting in June, but the discussion was anything but a snooze fest. New Fed Chair Kevin Warsh moved quickly to signal change, announcing the formation of five task forces focused on reviewing different aspects of the Fed’s framework and announcing the removal of traditional forward guidance. While the Summary of Economic Projections (dot plot) will remain in place, the Fed chair’s individual projections will no longer be included. Despite that shift, the message from the dot plot was still interpreted as hawkish. The 2026 projection now shows nine members expecting the federal funds rate to move higher during the year. Markets reacted with front-end yields increasing. Inflation remains elevated globally, particularly at the headline level, on the back of elevated energy prices. This prompted the European Central Bank (ECB) and the Bank of Japan (BOJ) to raise interest rates, with the latter moving rates to the highest level since 1995. Nonetheless, If the Iran-U.S. peace deal holds, energy prices may further stabilize, which could help bring down near-term inflation readings. At the same time, with growth concerns in the U.K., Europe, and Canada building, SEI believes that future monetary policy is more of a two-sided debate than the market is currently pricing. The resilience of the U.S. economy has been stronger than markets expected, leaving the Fed in a familiar but challenging spot, with above-target inflation alongside solid growth. This backdrop sits somewhat at odds with Warsh’s prior inclination toward lower rates. How he balances that view with real-time economic data, while keeping the Federal Open Market Committee (FOMC) aligned and maintaining market credibility, will be important to watch. SEI continues to expect that the Fed will remain on hold in the near term.

Federal Reserve (Fed)

• At Kevin Warsh’s first meeting as Federal Reserve (Fed) Chair on April 16-17, the Federal Open Market Committee (FOMC) voted unanimously (12-0) to maintain the federal funds rate in a range of 3.50%-3.75%. Warsh was sworn in as Fed chief on May 22, succeeding Jerome Powell, who still serves as a member of the Fed Board of Governors.

• In its statement announcing the rate decision, the FOMC noted the resiliency of the U.S. economy. “Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East,” the FOMC said. The Fed's so-called dot plot of economic projections indicated a median federal funds rate of 3.8% at the end of 2026, up from its forecast of 3.4% in March, signaling that the central bank anticipates one rate hike this year.

• During a news conference on Wednesday afternoon following the FOMC meeting, Warsh said that the central bank did not consider a rate cut. “There was one proposal on the table, there was no discussion of any other proposals,” he commented. Warsh also noted that the Fed provided little forward guidance for policy because it is “not well suited to the current policy conjuncture.”

European Central Bank (ECB)

• The ECB voted unanimously to raise its benchmark interest rate by 25 basis points (0.25%) to 2.25% at its June 10-11 meeting, citing the Mideast conflict’s impact on the European economy.

• In a news release, the ECB’s Governing Council commented, “The outlook remains uncertain, with upside risks for inflation and downside risks for economic growth. The full implications of the war for medium-term inflation and growth will depend on the intensity and duration of the energy price shock, as well as the scale of its indirect and second-round effects.”

• In prepared remarks for a news conference following the rate announcement, ECB President Christine Lagarde and Vice President Boris Vujčić said, “The risks to the growth outlook are to the downside, mainly owing to the war in the Middle East, which has added to the volatile global policy environment. Prolonged disruption of energy supplies could increase energy prices further and for longer than currently expected. These factors would erode real incomes even more and make firms and households more reluctant to invest and spend.”

Bank of England (BOE)

• At its meeting on June 17, the BOE voted by a margin of 7-2 to maintain the Bank Rate at 3.75%, citing the impact of the ongoing Mideast war. Monetary Policy Committee (MPC) members Megan Greene and Huw Pill supported a 25-basis-point (0.25%) rate increase.

• The MPC stated, “Global energy prices have fallen since the previous meeting in response to events in the Middle East. But they remain higher than pre-conflict and have continued to be volatile. The impact of the energy shock on the U.K. economy remains uncertain. Monetary policy cannot influence energy prices but is being set to ensure that the economic adjustment to them occurs in a way that achieves the 2% inflation target sustainably.”

• The central bank’s announcement provided insights into the views of the MPC members. BOE Governor Andrew Bailey said, “There has been a marked fall in energy prices in recent days, reflecting progress on talks involving U.S. and Iran. But the situation remains unpredictable, and there is clearly a risk that energy prices remain elevated for an extended duration. Recent inflation outturns give greater confidence that gradual underlying disinflation has continued.”

Bank of Japan (BOJ)

• At its meeting on June 15, the BOJ voted by a 7-1 margin to raise its benchmark interest rate by 25 basis points (0.25%) to a 31-year high of 1.00%. Board member Asada Toichiro favored maintaining the rate at 0.75%. BOJ Governor Kazuo Ueda did not attend the meeting as he was undergoing medical treatment.

• In a statement announcing the rate decision, the central bank commented, “While higher crude oil prices have been exerting downward pressure on economic activity, the economy has generally been supported by factors such as high levels of corporate profits and an improvement in the employment and income situation. Meanwhile, the risk of a significant slowdown in the economy appears to have decreased compared with a while ago.”

• At a news conference following the meeting, BOJ Deputy Governor Shinichi Uchida noted that the BOJ could implement additiional rate hikes if inflation pressures do not subside, “With underlying inflation approaching 2%, we need to be mindful of upward price risks. We will guide policy so that we won't fall behind the curve,” he said.

Bank of Canada (BOC)

• The BOC maintained its policy rate at 2.25% following its June 10 meeting.

• In a statement announcing the monetary policy decision, the central bank noted the economic impact of the ongoing Mideast conflict as well as U.S. trade policy. “The resulting increases in energy prices and disruptions in global supply chains are weighing on global economic growth and pushing up inflation,” the BOC stated. “At the same time, the U.S. administration continues to propose new tariffs, and trade policy uncertainty remains elevated.”

• At a news conference following the interest-rate announcement, BOC Governor Tiff Macklem commented that the BOC is waiting to see if higher energy prices lead to a broader rise in inflation. “Economic weakness combined with rising inflation is a dilemma for monetary policy,” he said. “Raising rates to dampen inflation could further slow the economy. Easing rates to support growth increases the risk that higher inflation becomes persistent. For now, holding the policy rate unchanged balances those risks.”

GLOSSARY AND INDEX DEFINITIONS

For financial term and index definitions, please see: https://www.seic.com/ent/imu-communications-financial-glossary

IMPORTANT INFORMATION

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results,

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting, and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI). Information in Canada is provided by SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company (SEI), and the Manager of the SEI Funds in Canada. In the UK and the EEA this information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document has not been registered as a prospectus with the Monetary Authority of Singapore.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.