Central bank depository.

SEI’s View

Policy rates in the advanced economies will likely ease further in 2025. SEI is not convinced that it is necessary for the U.S. to “follow the crowd.” Some members of the Federal Open Market Committee (FOMC), the policy decision-making arm of the Federal Reserve, now appear to be having second thoughts as well. Although the central bank reduced the federal-funds funds

rate in December, its accompanying rhetoric and the new projections published in the aftermath of the meeting shifted significantly. The Bank of England kept its Bank Rate unchanged in December, but there were three dissenters who wanted to reduce the rate. In contrast, the pressure on the European Central Bank to adopt an aggressively easy monetary policy will

become more intense if a trade war with the U.S. materializes.

U.S. Federal Reserve (Fed)

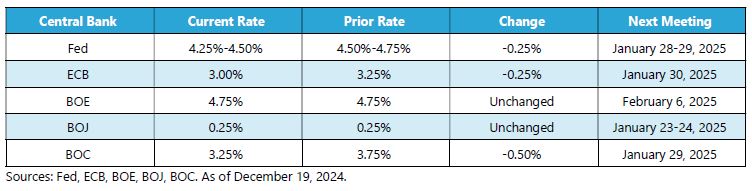

- By an 11-to-1 margin, the FOMC voted to reduce the federal-funds rate by 25 basis points (0.25%) to a range of 4.25% to 4.50% following its meeting on December 17-18. Cleveland Federal Reserve President Beth Hammack voted to maintain the target rate in a range of 4.50% to 4.75%.

- In a statement announcing the rate decision, the Committee stated that, in considering further rate cuts, the Committee members will "carefully assess incoming data, the evolving outlook, and the balance of risks."

- The Fed’s so-called dot plot of economic projections indicated a median federal-funds rate of 3.9% at the end of 2025, up from its previous estimate of 3.4% issued in September, signaling that the central bank anticipates federal-funds rate cuts totaling roughly 0.50% by the end of next year. The central bank’s previous dot plot had projected that the benchmark rate would decline 1.0% in 2025.

- The Fed estimated that core inflation, as measured by the core personal-consumption-expenditures (PCE) price index, will rise by an annual rate of 2.5% next year—modestly higher than the central bank’s 2.2% forecast in September. The personal-consumption-expenditures (PCE) price index is widely considered the Fed’s preferred measure of inflation as it measures the prices that consumers pay for goods and services to reveal underlying inflation trends.

European Central Bank (ECB)

- The ECB reduced its benchmark interest rate by 0.25% to 3.00% on December 12—its fourth rate cut over its past five meetings. The ECB previously implemented rate cuts of 0.25% in June, September, and October—the first reductions since September 2019.

- In a news release announcing the rate decision in December, the ECB’s Governing Council stated that it is “determined to ensure that inflation stabilises sustainably at its 2% medium-term target.” The central bank did not include the wording in its previous statement in October that it intended to “keep policy rates sufficiently restrictive for as long as necessary to achieve this aim.”

- The ECB noted that recent data indicate “inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis. Domestic inflation has edged down but remains high, mostly because wages and prices in certain sectors are still adjusting to the past inflation surge with a substantial delay.”

Bank of England (BOE)

- In a split vote at its meeting on December 18, the BOE maintained the Bank Rate at 4.75%. Three BOE Monetary Policy Committee (MPC) members voted for a 0.25% rate cut.

- In its announcement of the rate decision, the MPC appeared to take a somewhat hawkish tone, commenting that ”wage growth and some indicators of inflation expectations had risen, adding to the risk of inflation persistence.”

- The MPC also noted that it is “monitoring the impact on growth and inflationary pressures from the measures announced in the Autumn Budget [for 2024], and from geopolitical tensions and trade policy uncertainty. These developments have generated additional uncertainties around the economic outlook.”

Bank of Japan (BOJ)

- By an 8-to-1 margin, the Bank of Japan (BOJ) left its benchmark interest rate unchanged at 0.25% at its meeting on December 18-19. The central bank has been on hold since it raised the rate from 0.1% to 0.25% following its meeting at the end of July. One BOJ Policy Board member voted for a 0.25% increase to 0.50%, due to concerns about signs of increasing inflationary risks.

- In a statement announcing the rate decision, the BOJ noted that “services prices have continued to rise moderately, reflecting factors such as wage increases, although the effects of a pass-through to consumer prices of cost increases led by the past rise in import prices have waned. Inflation expectations have risen moderately.

- During a news conference following the meeting, BOJ Governor Kazuo Ueda commented that the central bank will be monitoring the labor market and assessing the possible impact of U.S. President-elect Donald Trump’s trade policies on Japan’s economy. "Taken together, the likelihood of Japan's economy moving in line with our forecast is heightening. But we'd like one notch more information to believe we can raise interest rates. That includes the sustainability of wage increases," Ueda said.

Bank of Canada (BOC)

- The BOC cut its policy rate by 0.50% to 3.25% following its December 11 meeting. In total, the central bank has reduced the rate by a full percentage point at its last two meetings.

- However, the BOC cautioned that it may slow the pace of its monetary policy easing. In its news release, the central bank stated that it “will be evaluating the need for further reductions in the policy rate one decision at a time. Our decisions will be guided by incoming information and our assessment of the implications for the inflation outlook.”

- The BOC also noted that the possibility of new tariffs imposed on Canadian exports by the incoming U.S. presidential administration of Donald Trump, who will take office on January 20, “has increased uncertainty and clouded the economic outlook.”

Other central banks

- The Swiss National Bank (SNB) reduced its benchmark interest rate by 0.50% to 0.50% following its meeting on December 12, exceeding market expectations of a 0.25% cut. The SNB projects that the average annual inflation rate will end 2024 at 1.1%, moderate to 0.3% in 2025, and then rise to 0.8% in 2026. In response to the rate-cut announcement, the Swiss franc briefly declined to a two-week low against the euro before rebounding later in the day.

Summary Table

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

In the UK and the EEA this information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document has not been registered as a prospectus with the Monetary Authority of Singapore.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.