Asset Allocation: Low-Volatility Equities in a Diversified Portfolio

The merits of low-volatility investment strategies have been understood for quite some time. In fact, SEI helped pioneer the approach, having launched our first strategy in the space in 2004—after our own research1 found that lower-volatility stocks not only experience considerably less volatility and lower declines than equities as a whole, but also may even deliver market-like returns over time.

We have found this makes low-volatility equities particularly attractive for investors who care primarily about absolute risk, meaning they are more concerned about the risk of losing money than the risk of underperforming a market index. For example, individuals focused on avoiding losses exceeding a certain amount (say, 10% or 20% of the portfolio’s value), may find low-volatility strategies especially compelling.

However, the utility of low-volatility strategies can extend beyond the most conservative portfolios. Even the most aggressive investors may benefit from an allocation that’s designed to dampen portfolio volatility.

Why isn’t everyone investing in low-volatility strategies?

While low-volatility equities generally exhibit low absolute risk, they can sometimes outperform or underperform by large margins for an extended period of time. Therefore, not everyone is necessarily comfortable with that divergence when it happens in their portfolios.

Such anxiety is natural during periods of market stress. However, if an investor’s asset allocation decisions are based on achieving a certain financial goal—retirement, college tuition, a vacation home, or some other spending objective—then the risk of gain or loss relative to the market would not be relevant. Imagine, for example, that an investor’s portfolio is up 20% while the market is up 25%—yet the portfolio only requires 6% to achieve its objective. It may be lagging the market, but the portfolio is clearly well ahead of expectations in terms of achieving the investor’s goal. And, in our view, it’s more appropriate to measure the success of a goals-based portfolio in terms of achieving its given objective rather than outperforming the market.

This is not always the case. Unfortunately, most investors have been conditioned to judge the success of their portfolios against benchmark indexes instead of in relation to their personal goals. This is due to many professional money managers being compensated based on performance relative to the benchmark. In other words, if their portfolios underperform, their compensation declines; if their portfolios outperform, their compensation goes up—indirectly incentivizing them to reduce the volatility of their performance and create portfolios that look similar to benchmarks in an effort to reduce the volatility of their compensation.

When boring is better than the lottery

Another likely reason that investors have not universally adopted low-volatility investing is that most are drawn to trades that appear to offer dazzlingly high potential short-term outcomes. Many also appear willing to pay a premium for the thrill of owning stock in companies that generate a lot of buzz—overpaying to invest in an exciting upstart electric-car company, for example, rather than underpaying for a well-established, highly profitable pharmaceutical company (compared what “rational” finance theory would indicate each company is worth). Rational finance theory assumes rational behavior on the part of individuals and that investors employ rational calculations to make rational choices and achieve outcomes that are aligned with their own personal objectives.

The temptation to chase “lottery-like” returns is understandable. However, these types of trades often come with higher risk and consequently lottery-like outcomes (a low-odds game).

We believe it is far wiser to adopt a more patient investing approach. Our research2 shows that investors willing allocate to unexciting companies—particularly when buying shares at bargain prices—will likely be rewarded in the form of higher risk-adjusted returns3 as the value of their “boring” investments slowly compounds over time.

Low-volatility equities and rising interest rates

Low-volatility equities exhibit a moderate amount of sensitivity or responsiveness to interest-rate changes, particularly over certain periods. But that’s not necessarily a bad thing.

First, timing interest-rate movements is just as hard as timing stock-price movements. It comes with higher risk. The 40-year bull market4 in bonds (during which U.S. Treasury bond market prices have moved higher) is proof that it’s not as simple as saying “interest rates are low so they have to rise”. Since we cannot predict the future, interest-rate exposure remains a valuable diversifier to equity risk.

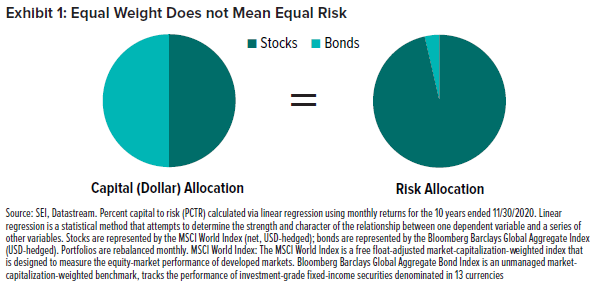

Second, it’s important to remember that even many traditional “balanced” portfolios have far less interest-rate risk than one may expect. In a 50/50 stock-bond portfolio, we can see that stocks account for more than 95% percent of the risk (Exhibit 1).

From this perspective, low-volatility equity’s combination of smaller contributions to relative returns and modestly higher interest-rate sensitivity isn’t a big concern in our view. If anything, it may bring a portfolio into better balance from a risk perspective.

Finally, it’s helpful to remember that the relationship between interest rates and equities varies throughout time. Recently, technology-related growth companies have dominated the markets; they are meaningfully “long duration5” in the sense that most of their earnings are projected well into the future. However, in the event that interest rates rise faster than expected, it’s far from clear that those technology-related growth stocks would outperform low-volatility stocks. That’s because applying higher rates to future earnings may well hurt long-duration stocks.

SEI’s view

While many equity-market crises share similar features, it’s important to realize that no two episodes are exactly the same. The selloff in 2020 was especially unusual given the economic circumstances created by a once-in-lifetime pandemic. At the time, safety measures including government-mandated lockdowns made it impractical, or even illegal for consumers to purchase certain goods and services through traditional (in-person) channels.

While most businesses were struggling in the early days of the pandemic, the few already-established masters at delivering products straight to consumers’ homes (such as major online retailers and on-demand entertainment providers) outperformed in this environment. Traditionally, these mega-cap6 technology names would not be expected to remain steady in such a volatile equity market; they had an unusual advantage because of the unique nature of the public health crisis. In a more typical equity selloff, we wouldn’t expect them to provide much of a cushion, if any, from losses.

More commonly, general economic weakness causes consumers to spend less and businesses to invest less, which leads to contractions in corporate earnings—particularly in more discretionary sectors. This is likely intuitive because discretionary spending is, by definition, non-essential—and, therefore, the easiest expense for consumers and companies to cut back on. Unfortunately, low-volatility stocks faced headwinds in this environment.

The good news is that low-volatility equities have performed remarkably well in just about every other market selloff in recent memory.7 While we can’t know anything for certain about the next crisis, history suggests that 2020 was an exception—not the “new normal”—and that low-volatility equity investments should continue to help mitigate losses in the vast majority of market drawdowns going forward.

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change.

This material may contain “forward-looking information” (“FLI”). FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments and the use of an asset allocation service. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.