Are Investment-Grade Bonds Still Worth Holding?

With investment-grade bond yields at historic lows, it’s not surprising to hear investors express concerns about the effectiveness of fixed-income allocations in a strategic portfolio. Some investors have even questioned whether it’s time to abandon investment-grade bond allocations altogether. While an understandable consideration given the historically low rates and narrow spreads, our answer is a resounding ‘No.’

We believe that investment-grade bonds will continue to offer a combination of better returns than cash (positive risk premium) and genuine diversification benefits relative to equities. In our view, those diversification benefits are particularly notable since equity risk typically dominates investors’ portfolios. If the economic recovery out of the current pandemic were to falter, we think exposure to bonds could help mitigate harm caused by a drop in stock prices. On the other hand, if economic growth strengthens, we would expect investment-grade bonds to hold their value given the outlook for continued low interest rates as a result of efforts by global central banks to support the economic recovery.

Let’s take a closer look at investment-grade bonds both as a standalone investment and as a component of a diversified portfolio.

Asset-class risk: standalone investments

When considering investment-grade bonds as a standalone investment, an increasingly common fear among investors is that low interest rates (which result in low yields) will undermine their investment from both risk and return perspectives. Put another way, investors are questioning whether the now-paltry expected returns are worth the usual risk that a bond issuer may default and fail to repay the loan. We would make the case that the expected return relative to stocks appears unchanged and, therefore, the relative attractiveness of each asset class remains the same.

There is no clear indication that return assumptions today are any different than they have always been—with investment-grade bonds (as measured by the Bloomberg Barclays Global Treasury Index and Bloomberg Barclays Global Aggregate ex-Treasury Index) historically expected to return about 1% to 2% more than cash (the return on cash is often referred to as the short-term risk-free rate) on an annualised basis, and stocks (as measured by the MSCI ACWI Index) expected to return roughly 5%-6% more than cash. In addition to risk premiums (excess return expectations above the cash rate) remaining the same, expected total returns (the return that includes interest payments and changes in principal) have lowered across all asset types at roughly the same pace. This would imply that the relative attractiveness of each asset class remains the same; that is, the rewards for taking risk, over and above the risk-free rate, have not significantly changed.

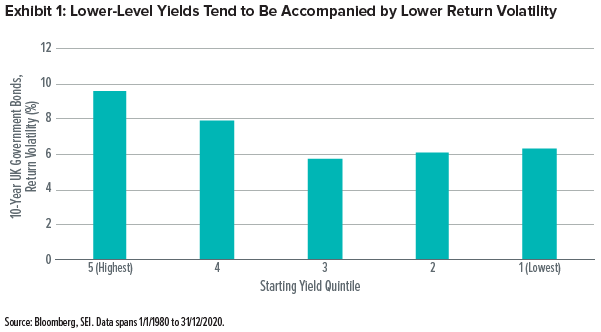

With seemingly nowhere to go but up, do low interest rates mean bond returns will be more volatile than they have been historically as rates begin to rise? We can assess this by examining interest-rate risk, a measure of potential portfolio losses when interest rates rise that is a function of both duration and the volatility of yields themselves. History suggests that while lower rates imply higher duration, yield volatility actually tends to decline as the level of yields declines. Exhibit 1 illustrates this point using 10-year UK Government bonds as an example; similar experiences can be seen in bond markets throughout the developed world.

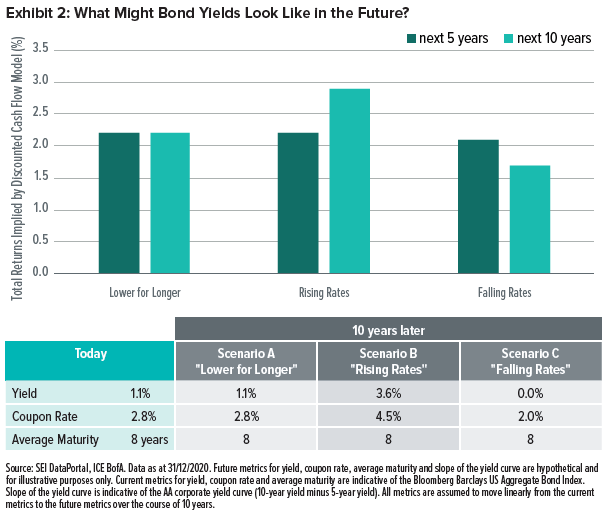

While a sharp move higher in yields would reduce bond prices in the near term (prices and yields have an inverse relationship), it would also improve the reinvestment outlook (as bonds mature, investors can purchase new bonds that offer a higher rate of interest) and increase expected longer-term returns. Exhibit 2 utilises US data (based on the better availability of historical data), but we believe the chart illustrates concepts that transcend geography. Perhaps somewhat counterintuitively, a rising-rate environment could be the most beneficial of the potential outcomes over a longer-term horizon.

Portfolio risk

When rates fall further and further, fixed-income returns are often challenged. As the price of a bond climbs higher, the fixed coupon payment (paid to investors in the form of interest) becomes smaller by comparison. This leaves investors subject to “reinvestment risk”—that is, when proceeds from maturing bonds are reinvested in a less favourable environment of higher prices and lower yields. Investors in this scenario commonly wonder whether bonds are too richly valued to fill their traditional role of portfolio diversifier.

However, in a world of low or negative short-term interest rates, we believe it is reasonable to view valuations as elevated across all financial assets (including stocks and bonds). As a result, forward-looking expected returns would likely be lower across the board—not just for fixed-income investments. So the question then becomes, “Are correlations between bonds and riskier assets such as equities still low enough toprovide diversification benefits?”

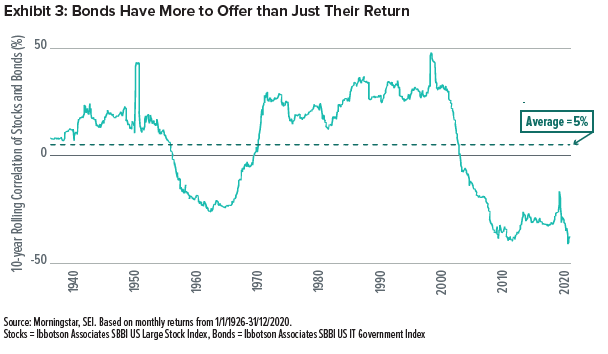

Historical data show that the correlation between bonds and equities tends to remain low in periods of stress—and, in many cases, actually falls. As in the previous chart, we utilise US data (based on the better availability of historical data) for Exhibit 3. We believe this demonstrates that investment-grade bonds are one of the few asset classes that are genuinely diversifying to equities.

Diversification: First, Last, Always

We realise low yields don’t excite anyone. We are also well aware that diversified portfolios are unlikely to make the list of the year’s top performers. Still, we firmly believe that seeking to maximise returns and minimise risks is the right way to approach portfolio construction. Accordingly, we’ll be holding on the bonds in our strategic allocations.

Glossary of Financial Terms

Duration: The change in a bond’s price given a change in interest rates.

Index Definitions

Bloomberg Barclays Global Treasury Index: a broad-based measure of fixed-rate, local-currency government debt of investment-grade countries, including both developed and emerging markets.

Bloomberg Barclays Global Aggregate ex-Treasury Index: a broad-based measure of the global investment-grade fixed-rate debt markets outside of the US.

Bloomberg Barclays US Aggregate Bond Index: a benchmark index composed of US securities in Treasury, government-related, corporate and securitised sectors. It includes securities that are of investment-grade quality or better and have at least one year to maturity.

Ibbotson US Large Company Stock Index: a benchmark index that measures large company stocks. It is represented by the S&P 500 Composite Index (S&P 500) from 1957 to present, and the S&P 90 from1926 to 1956.

Ibbotson US Intermediate-Term Government Bond Index: a benchmark index that is measured using a one-bond portfolio with a maturity near five years.

MSCI ACWI Index: a capitalization-weighted index that is representative of the market structure of 46 developed- and emerging-market countries in North and South America, Europe, Africa, and the Pacific Rim.

Important Information

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments.

Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all of the risks applicable to our funds, please refer to the fund’s Prospectus.

Please contact your fund adviser (South Africa contact details provided above) for this information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.