Alternative Investments in a Rising-rate Environment

Alternative investments provide broad exposure across areas of the financial markets that would otherwise be absent in a typical portfolio. These exposures can enhance portfolio diversification and seek to improve the overall risk-reward profile for an investor. As alternatives are not perfectly correlated with traditional asset classes like equities and fixed income, incorporating them into asset-allocation strategies can increase expected returns for given levels of risk or decrease the level of risk for a given level of return.

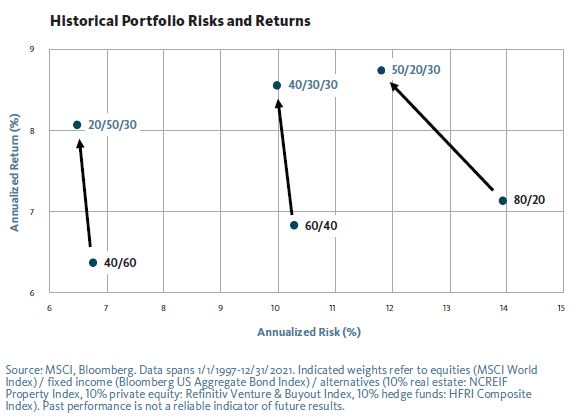

The following exhibit visualizes the historical benefit of adding alternatives to an investor portfolio of equities and fixed income: increased returns with lower annualized volatility.

We believe the distinct set of strategies offered by alternative investments can broaden the diversification opportunities beyond those available via traditional investments, thereby helping to improve upon the limited risk-reduction and return-enhancement opportunities that traditional asset classes can offer

The impact of rising rates

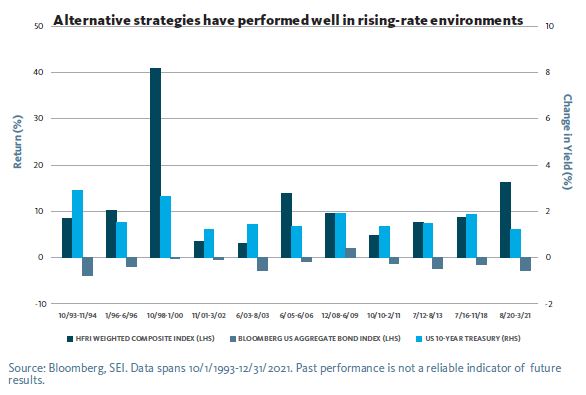

Rising bond prices and falling yields have been the norm in fixed-income markets over the past four decades. The U.S. three-month Treasury bill yielded near 0% at the end of December, while the yield on U.S. 10-year Treasurys was around 1.5% (after falling near 0.5% at the start of the pandemic). As the U.S. economy displays signs of significant economic growth, the Federal Reserve (Fed) has maintained that it could withdraw accommodative policy action and eventually allow interest rates to normalize across the yield curve.

We examined previous spikes in interest rates since 1990 when the yield on U.S. 10-year Treasurys increased by 1% or more. During each period, alternative strategies (as measured by the HFRI Weighted Composite Index—a global index designed to measure the performance of the largest hedge funds) delivered positive absolute performance; the Bloomberg US Aggregate Bond Index fell in each period but one, highlighting the benefit of alternatives within a diversified portfolio.

Higher interest rates should support the following strategies within the alternatives asset class:

- Long/short equity: the yield on short-term cash lending can provide a boost to long/short equity returns. As we move to a more normalized interest-rate environment, we expect these strategies to benefit from the compounding of higher rates.

- Merger arbitrage: the potential profit (called the spread) is composed of a risk premium plus the risk-free rate. All other considerations being equal, an increase in the risk-free rate will therefore result in wider spreads and potentially greater returns.

- Managed futures and global macro strategies: managed futures fund managers are generally required to post little collateral on futures contracts, allowing them to invest most of a fund’s assets in U.S. three-month Treasurys. Therefore, the performance of these strategies is directly impacted by the level of short-term interest rates.

- Thematic investing: funds positioned for higher rates or built around potential inflection points in inflation will benefit.

- Core property strategies can benefit as property values and rental income will tend to rise in an inflationary environment that is also characterized by a strong economy.

- Structured credit should benefit from higher yields as the interest charged on loans generally increases with rising short-term benchmark rates, a characteristic that increases inflation protection.

By broadening the diversity of an overall portfolio with alternative strategies and aligning them with the goals they’re best suited to achieve, we believe investors can build more efficient portfolios and improve their risk-adjusted returns. In an environment of higher rates, we see the promise for alternative investment strategies to further expand the opportunity-set for generating returns.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. Diversification may not protect against market risk. Alternative investments involve a high degree of risk and can be illiquid due to restrictions on transfer and lack of a secondary trading market. They can be highly leveraged, speculative and volatile. Please ensure you are aware of the risks before investing.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.