After the attack: What comes next?

The U.S. attack on Iran’s nuclear facilities has significantly increased geopolitical risk, raising concerns about oil prices and the potential for escalating military conflict. Short-term disruption aside, we believe the profound changes in the political dynamics in the Middle East should play to the advantage of the U.S. once the dust settles.

Geopolitical risk has taken a leap forward now that America has entered the fray. While there is always the chance that Iran will lash out and disrupt shipping through the Strait of Hormuz or attack some oil-producing and refining facilities and export terminals in the neighboring Gulf States, we see this as a low-probability event for more than one reason:

- Iran cannot disrupt its neighbors’ exports without disrupting its own; some 95% of Iran’s oil exports are loaded onto tankers docked at Kharg Island, which is near the northern end of the Persian Gulf: In addition

- Iran cannot afford to lose friends, especially its most powerful friend; China is one of Iran’s strategic partners, receiving almost half of its imported oil from the Middle East.

Even in a worst-case scenario, in which some sort of supply blockage occurs, SEI assumes that it wouldn’t last long. Such a move by Iran also would give the U.S. justification to retaliate and do even more damage, this time to economically important assets. Oil prices may jump sharply, but the rise would likely be ephemeral. There is plenty of excess capacity to replace Iranian production.

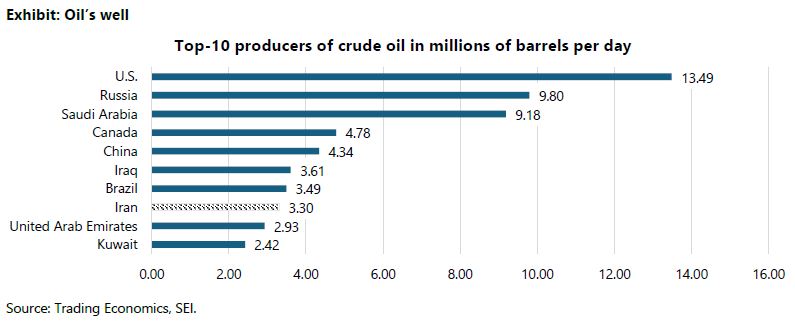

The exhibit below provides a list of the 10 largest producers of crude oil. Iran produces about 3.3 million barrels of oil per day, of which only about two million barrels are exported. Saudi Arabia alone has enough idled capacity to replace any Iranian crude taken off the market.

What’s next?

A more concerning issue following the attack on Iran’s key nuclear facilities by the U.S. is the possibility of attacks against U.S. military personnel and assets in the surrounding countries. Terrorist activity targeting soft targets in Europe and America itself cannot be ruled out either under this scenario. One thing is clear, however: Iran’s nuclear ambitions have been dealt a severe blow. The regime’s foreign-policy strategy also is in tatters following the military setbacks endured by Hamas and Hezbollah and the fall of the Assad regime in Syria. The nation’s ability to defend itself against Israeli attacks has been severely degraded to being nearly non-existent. It may not have any choice but to capitulate to U.S. demands and agree to a highly intrusive oversight of its nuclear program.

There is also the possibility of a regime change. No one can be sure what that would look like. Unfortunately, regime change in a repressive state like Iran can be a messy affair as different groups vie for power. The Revolutionary Guard probably is in the best position to take over the country given its military and economic power. We would not be surprised if the country remains an implacable enemy of Israel and the U.S. The big difference is that Iran’s nuclear program has suffered a significant setback. Taken as a whole, the profound changes in Middle East political dynamics should play to the advantage of the U.S. once the tension settles.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the investment fund manager and portfolio manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).