From 10 days of war to 10 years of inflation?

Over the last 10 days, the extent to which investor portfolios have been exposed to events related to the Russia/Ukraine conflict has trumped more traditional style factors, but it is still possible to draw some conclusions from the relative performance of factor returns.

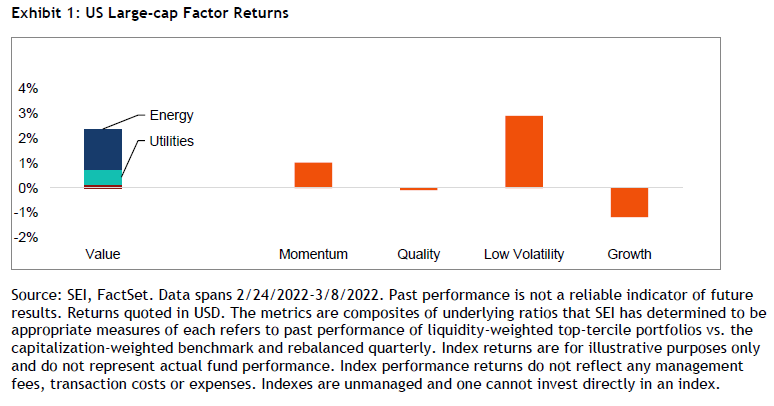

As shown in Exhibit 1, since Russia invaded Ukraine on 24 February 2022, value (as measured by the SEI Value Factor Family) has been defensive in the US and has been helped by exposure to the energy and utilities sectors, which have risen in tandem with surging oil prices.

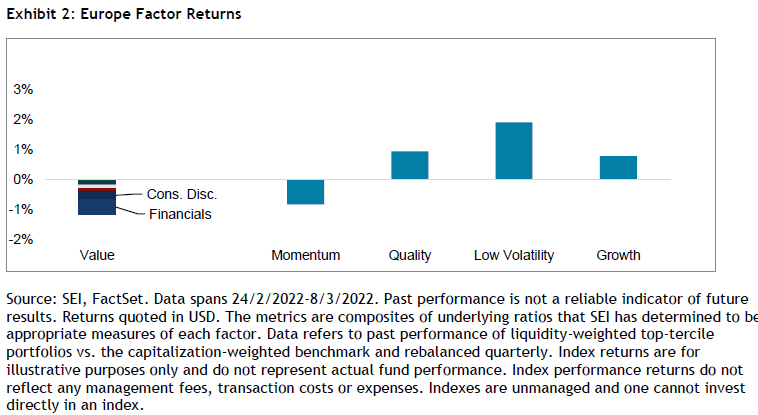

As shown in Exhibit 2, however, the value style in Europe has lagged, and the factor has been pulled down by declines in European banks and autos. Indirect exposure to Russia has been higher in Europe than in the US. 7.7% of European company revenues represented in the value factor portfolio are exposed to countries bordering Russia and Ukraine, while only 2.5% in the US value factor portfolio are similarly exposed.

We believe that the value lag in Europe is likely to be transitory, as the initial impacts of the conflict appear to have been absorbed and should ameliorate as inflationary tailwinds set in. Low-volatility has also benefited in both the US and Europe; the factor has helped cushion to the downside, behaving as expected as investor seek to reduce exposure to risker securities in their portfolio.

Spillover Effects

We believe investors should focus on the indirect impacts of the conflict, rather than any direct Russian exposures; these are far more impactful on portfolios:

- Knock-on effects of commodity price spikes feed into inflation.

- Sanctions result in supply-side disruptions and heightened economic uncertainty.

- Central banks have not dealt with elevated and persistent inflation for decades; printing money may now be unpalatable.

The Spectre of Stagflation

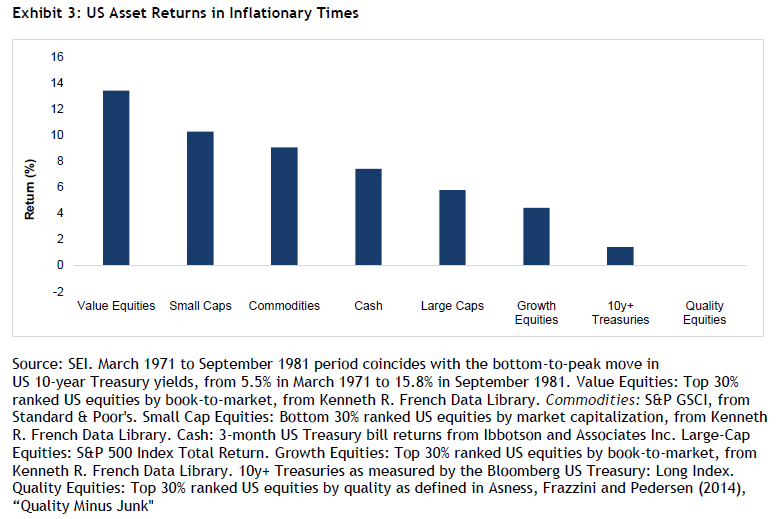

The current environment is beginning to compare to the stagflationary 1970s, a decade of significant and protracted inflation, fiscal and monetary instability, price controls, oil price spikes, and the Cold War. The period was a struggle for long-duration assets, including growth equities and long-maturity bonds, as shown in Exhibit 3.

Industries which lagged during this period include those sensitive to the end-consumer versus "Old Economy" beneficiaries of higher commodity prices1.

Our outlook

Although the immediate effects of the war are likely to subside, elevated inflation is likely to persist far longer. We believe long-duration assets, including government bonds and growth equities, are likely to suffer the brunt of the performance impact. Value and diversity are natural beneficiaries from rising costs and should perform well in an inflationary environment.

Glossary

Growth stocks exhibit earnings growth above that of the broader market.

Long-duration assets are those that are expected to deliver a higher proportion of their future cashflows in the long term.

Low-volatility refers to stocks that are less volatile than the broader market.

Momentum refers to a trend-following investment strategy that is based on acquiring assets with recent improvement in their price, earnings, or other relevant fundamentals.

Quality refers to a long-term buy and hold strategy that is based on acquiring assets with superior and stable profitability with high barriers of entry.

SEI Value Factor Family is a composite index of underlying ratios that SEI has determined to be appropriate measures of the value factor.

Stagflation refers to an economic environment of slow growth, relatively high unemployment, and rising prices.

Value refers to a mean-reverting investment strategy that is based on acquiring assets at a discount to their fair valuation.

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change. All information as of 30 May 2021.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The views and opinions within this document are of SEI only and are subject to change. They should not be construed as investment advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.