SEI Forward.

Market review

Global markets struggled during the last month of the quarter as the conflict in Iran and ongoing private credit troubles forced investors to reassess the outlook for global economic growth, the future path of monetary policy, and optimistic expectations for double-digit earnings growth. Equities reversed course during the quarter as fighting in the Middle East erupted, prompting the U.S. market to outperform the rest of the world in the downturn. The spike in energy costs and other commodities weighed on market performance as the energy sector was the lone positive in March and was the strongest performer during the quarter.

The severity of the selloff in global short-term yields was a bit surprising as investors priced in higher inflation and priced out any notion of central bank easing. Credit spreads widened on the growing private credit concerns which were further heightened as several high-profile funds gated investor redemptions.

Lastly, the U.S. dollar was among the few beneficiaries of a flight to safety, finishing the quarter in the green, while gold traded well off its all-time highs.

Tick tock, tick tock…

The onset of hostilities in the Middle East is the latest test for investors and the broader market as fears of a protracted conflict raise the specters of stagflation, recessions, and bear markets. The probabilities of all these outcomes have clearly increased as the supply disruptions in oil, fertilizers, helium, and other critical commodities extend the reach of this conflict well beyond energy and into other, crucial parts of the global economy, including agriculture and semiconductor production.

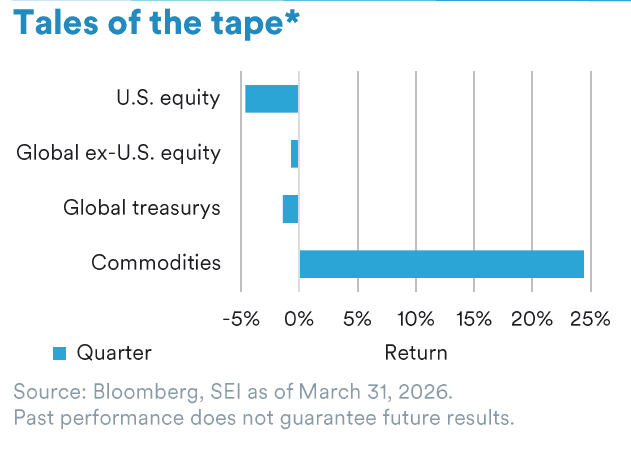

Notables for the quarter

- Oil; +78%: The Iran conflict has led to the closing of the Strait of Hormuz and destruction of key oil infrastructure in the Middle East.

- Gold; +8%: Despite a strong selloff in March, the shiny metal remains in positive territory for the year-to-date in 2026.

- Salesforce (ticker CRM); -30%: Will software providers remain relevant as AI use expands? The high concentration of software in private credit market fueled funding and default concerns.

- VIX level: Market volatility more than doubled in the quarter, exceeding 31 in late March before easing to 25.

While this war began as a conflict between the U.S., Israel, and Iran, the Iranian regime’s decision to target its Gulf neighbors in retaliatory strikes and the reality of the vital nature of the Strait of Hormuz to global supply chains, particularly in Asia, emphasizes that a resolution sooner rather than later is in a majority of the world’s best interests. The longer the strait is closed, the higher the probability of a poor outcome for both markets and the economy as the totality of the supply disruptions are significantly higher than any previous conflict in the region. Additionally, targeted strikes on infrastructure across the Middle East is another wildcard which may extend the consequences of this war well beyond any formal end to the hostilities as bringing supply back online will simply take time.

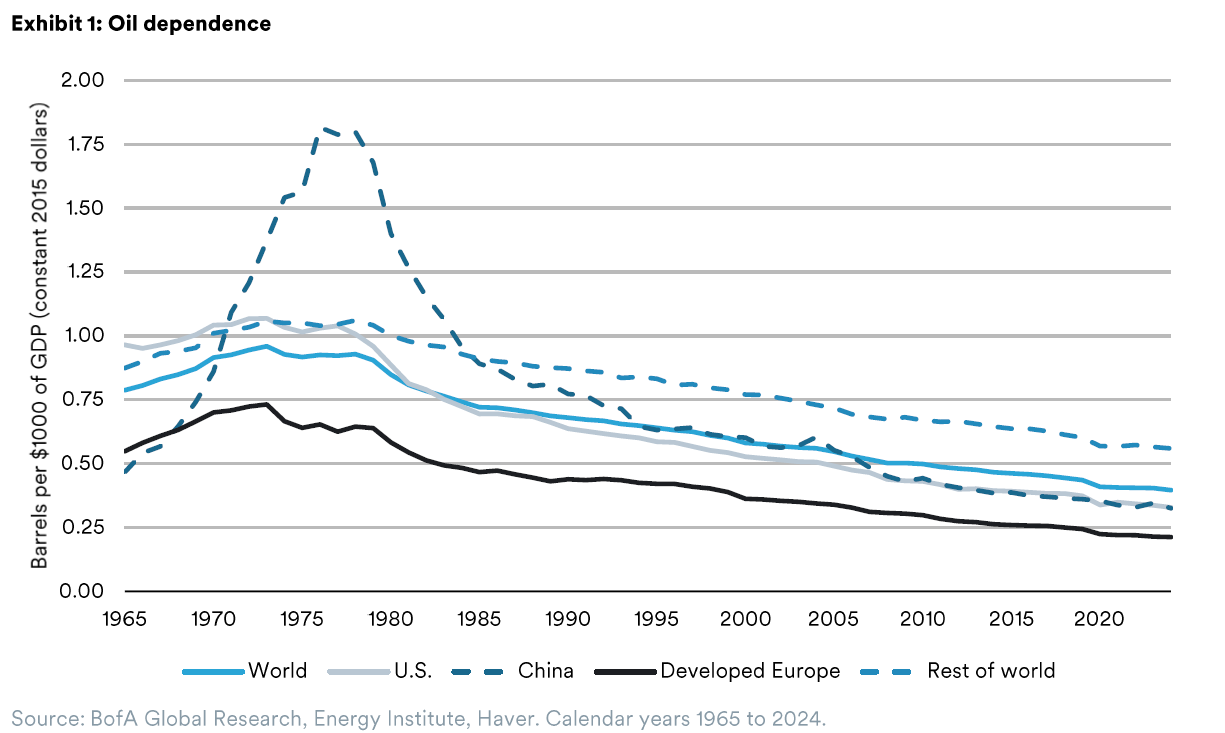

Despite all the challenges, a near-term resolution remains our base case, which suggests that this resilient global economy will avoid recession. Notably, the world is substantially less reliant on energy today than it was during prior conflicts. In fact, it requires about half as much oil to produce $1,000 of gross domestic product (GDP) today relative to the first Gulf War. In addition, the perilously critical role of the Strait of Hormuz in the global economy cannot be understated. This relatively narrow strait is responsible for the flow of 20% of global oil supplies and has been subject to the whims of the Iranian regime for the last 47 years. The fragility of that situation is, quite frankly, untenable and a resolution to this conflict, which includes the global economy no longer being held hostage to potential supply shocks by a hostile actor, is an enormously positive outcome.

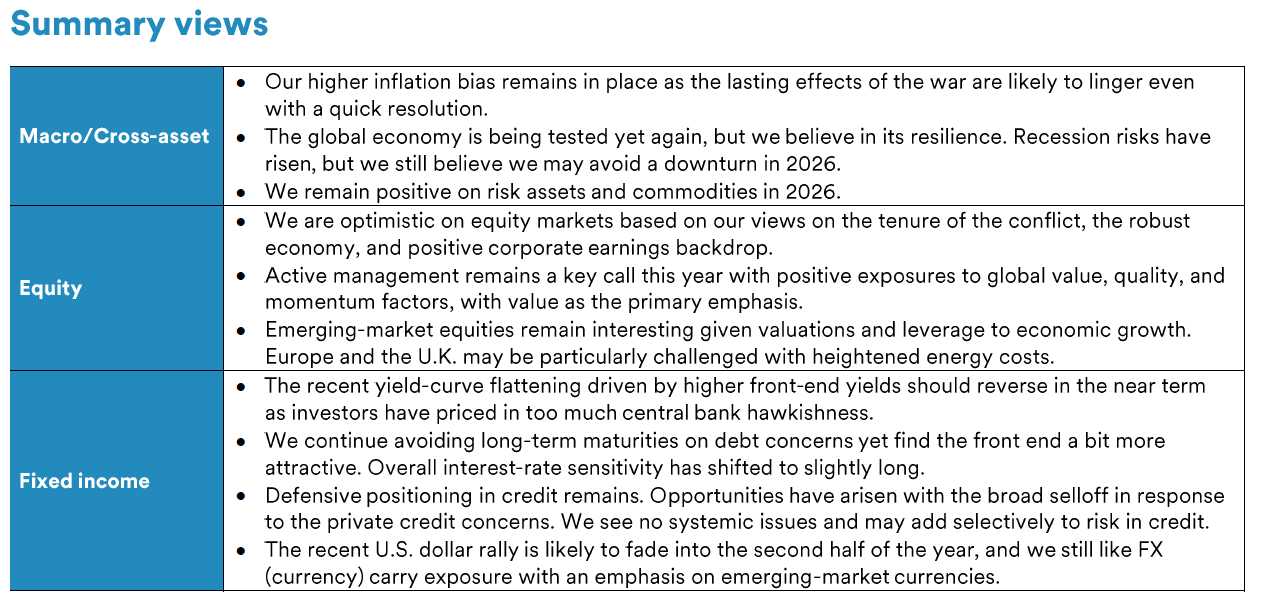

We remain constructive in our outlook for equities given our current views, including a near-term resolution to the conflict and the continued resilience of the economy and corporate earnings. Our strongest preference remains active management given the fluid situation in the Middle East and higher levels of stock-level dispersion. A value-oriented approach is a particular emphasis, and we expect continued outperformance for the remainder of the year. In addition, we still find emerging markets particularly attractive based on valuations and overall leverage to what we see as a still-growing global economy. Meanwhile, the current tensions raise the most concerns in Europe given the potential for an outsized economic impact from rising energy costs.

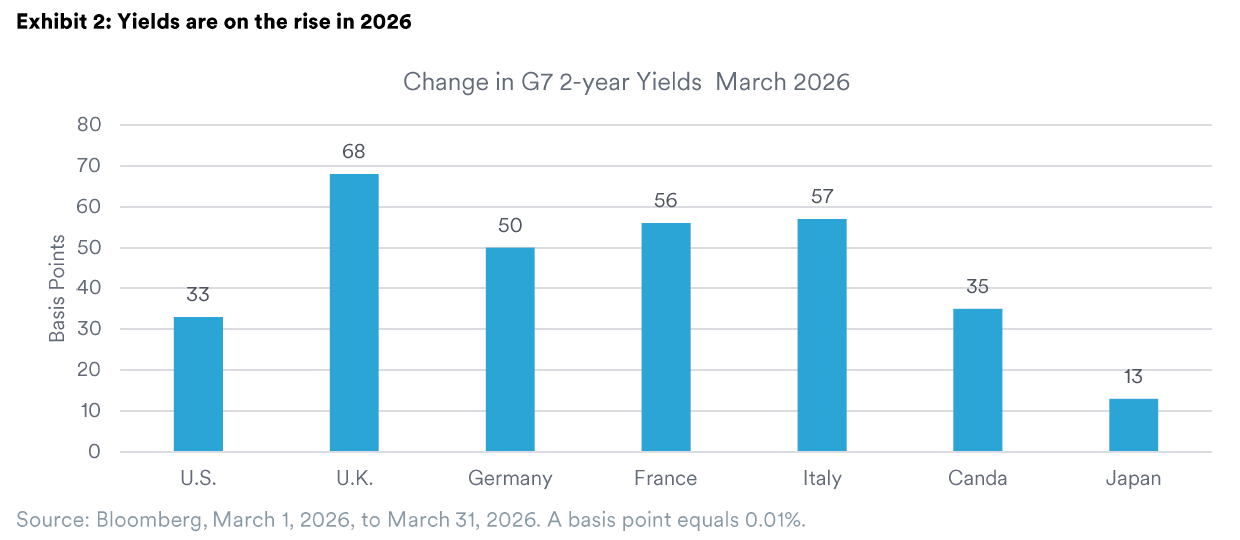

Fixed-income markets were particularly volatile in March as front-end yields sold off dramatically on inflation concerns from rising energy prices and expectations for tighter monetary policy. U.S. market expectations at the start of the year were for two full interest-rate cuts in 2026, which have now been fully priced out. Elsewhere, investors now expect multiple rate hikes, including from the Bank of England and European Central Bank. We view the severity of this move in yields to be a bit overdone as it will not be lost on monetary policymakers that higher overnight rates cannot open the Strait of Hormuz. Nonetheless, with inflation above most targets and rising, we do expect most central banks to adopt a more hawkish stance in the near term. Two-year yields look attractive at these levels, particularly in the U.S. We remain positioned for lower short-term rates on our expectations for less restrictive monetary policy than is currently priced in and positioned for neutral-to-higher long-term yields as the debt situation will only worsen with the onset of war.

Credit markets continued to digest private credit concerns as software companies became the latest “cockroaches” to emerge. Spreads in this sector widened as the future of software in an AI-enabled world was called into question. The gating of a few high-profile, retail private credit funds also grabbed headlines during the quarter as investors rushed for the exits. While we do believe that private credit is due for correction, we are confident that this will be relatively isolated. We simply do not see systemic contagion in this situation and no reflection of the leverage and breadth witnessed in the global financial crisis. Therefore, while we retain our defensive posture in credit markets, we are eager to take advantage of opportunities presented by this broader spread widening.

Commodity exposure was a bright spot for the quarter as broad indexes finished the quarter up nearly 25%. While energy was the key driver of the rally, agriculture including wheat and soybeans, and metals including aluminum, all finished substantially higher for the quarter. Precious metals are in positive territory for the year to date, but suffered in March as momentum in both gold and silver reversed dramatically. Commodities have been a key strategic and tactical position, and we remain positive on broad exposure. While we see a near-term end to the conflict as a likely outcome, the closure of the strait and the damage to infrastructure cannot be reversed immediately; therefore, we expect post-war energy prices to remain elevated for 2026. In addition, we believe that the selloff in gold seems overdone as we expect a resumption in demand from both investors and central banks.

Indexes

*Tales of the tape: U.S. equity: S&P 500 Index; Global ex-U.S. equity: MSCI ACWI ex-USA Index; Global Treasurys: Bloomberg Global Treasury Index; Commodities: Bloomberg Commodity Index.

Glossary and index definitions

For financial term and index definitions, please see: https://www.seic.com/ent/imu-communications-financial-glossary

Important information

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results. Diversification may not protect against market risk.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs, and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information in Canada is provided by SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company (SEI), and the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America, the Middle East, the Nordics, and Australia FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).