Monthly market commentary: Corporate earnings come back into focus.

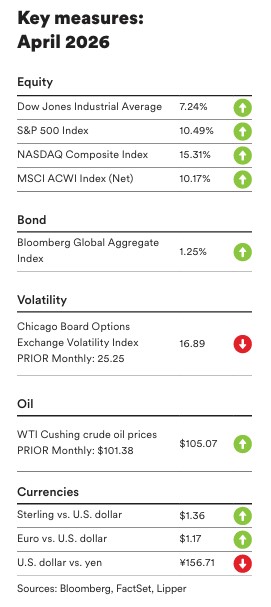

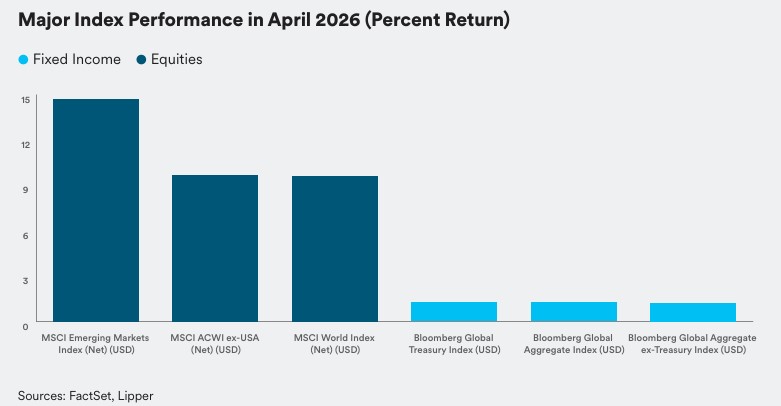

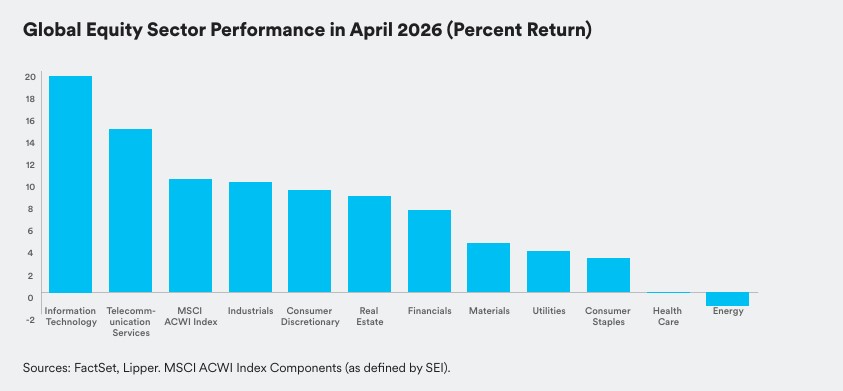

Global equities, as measured by the MSCI ACWI Index, rose sharply in April as investors were encouraged by relatively strong corporate earnings, particularly in the technology sector, as well as signs of easing geopolitical tensions in the Middle East. The markets were resilient against the backdrop of ongoing volatility and uncertainty surrounding the Mideast war, including Iran’s virtual closure of the Strait of Hormuz, a major shipping channel between the Persian Gulf and the Gulf of Oman. Emerging markets significantly outperformed developed markets for the month.

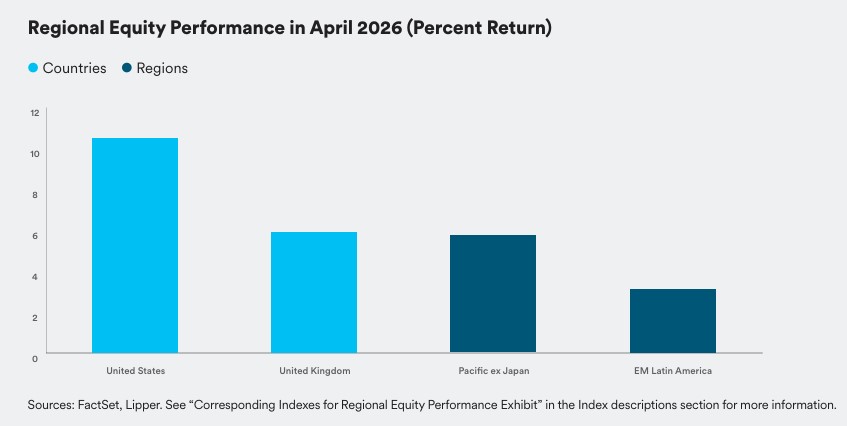

The Far East and Asia were the top performers among emerging markets in April, as both regions benefited from significant market rallies in Korea and Taiwan. Conversely, the Andean region within Latin America recorded a negative return and was the primary market laggard due to downturns in Colombia and Peru. The Gulf Cooperation Council (GCC) countries also underperformed amid weakness in Saudi Arabia. North America was the strongest-performing developed market for the month, bolstered by strength in the U.S. Additionally, both the Pacific and Far East regions benefited from strength in Japan. On the downside, the Pacific ex. Japan market underperformed due to relative weakness in Singapore.1

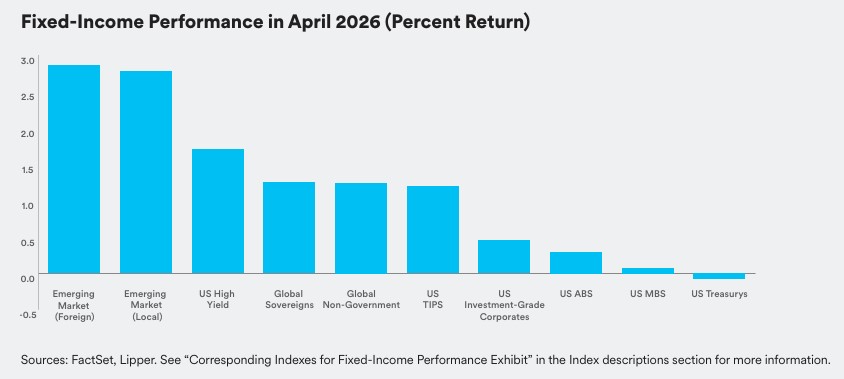

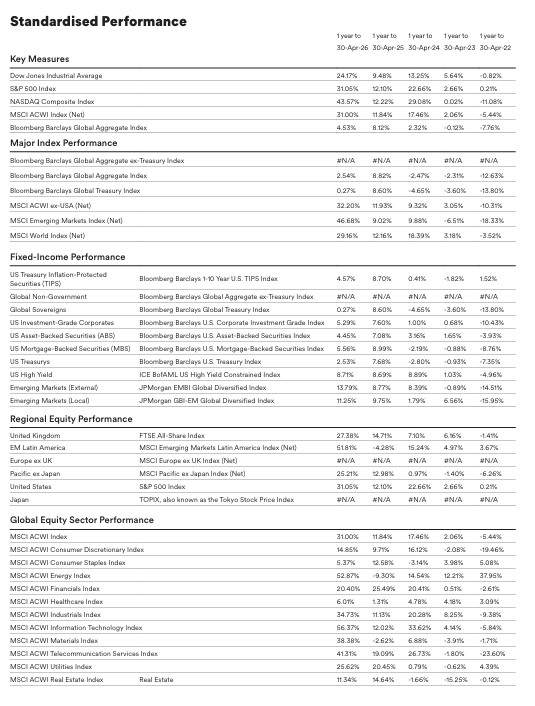

Global fixed-income assets, as measured by the Bloomberg Global Aggregate Bond Index, returned 1.3% (in U.S. dollars) in April. High-yield bonds led the U.S. fixed-income market, followed by investment-grade corporate bonds, mortgage-backed securities (MBS), and U.S. Treasurys. U.S. Treasury yields moved higher for all maturities of one year or greater and were flat to slightly lower in the shortest segment of the yield curve. (Bond prices move inversely to yields.) The yields on the 2-year Treasury note ticked up 0.09% in April to 3.88%, while 3-, 5-, and 10-year Treasury yields each rose 0.10%, ending the month at 3.91%, 4.02%, and 4.40%, respectively.2

Global commodity prices, as represented by the Bloomberg Commodity Index, climbed 4.2% in April. Oil prices maintained their upward momentum amid periods of volatility, with West Texas Intermediate (WTI) and Brent crude rising 3.6% and 6.2%, respectively, during the month due to uncertainty regarding the security of flows through the Strait of Hormuz. The gold price gained 1.1% in April as investors sought safe-haven assets amid the Mideast conflict, as well as inflationary concerns. The New York Mercantile Exchange (NYMEX) natural gas price declined 4.1% during the month as unusually warm spring weather in much of the U.S. dampened expectations for heating demand. The wheat price increased 3.3% in April in response to weather-related supply risks―particularly a drought in the U.S. and crop damage in the Black Sea region―as well Iran’s blockade of the Strait of Hormuz, which has impeded shipments of fertilizer.

On the geopolitical front, there were numerous twists and turns in the U.S.-Israel-Iran war in April. During a televised address on April 1, President Trump commented that the U.S. war effort in the Middle East was a success and the objectives of the military campaign would be completed in a short time. He dismissed risks to the U.S. economy and energy markets, and noted that the military operation was needed to deter the Iranian regime from enriching uranium to produce nuclear weapons.

Six days later, Trump announced in a social media post that the U.S., Israel, and Iran had agreed to a two-week ceasefire in the hostilities following the Pakistani government’s intervention. The U.S. initiated a retaliatory blockade of the Strait of Hormuz, a major shipping channel between the Persian Gulf and the Gulf of Oman, in mid-April in an effort to pressure Iran to stop interfering with shipping by preventing the country from exporting oil. The blockade applies only to ships entering or leaving Iranian ports. On April 21, one day before the ceasefire was scheduled to end, Iranian officials backed out of negotiations with the U.S., which were scheduled to be held in Pakistan. However, Trump announced that he would extend the deadline if Iran agreed to restart peace talks. Toward the end of the month, Iran (through intermediaries Pakistan and Oman) issued a proposal to reopen the strait and end the war. However, Trump rejected the offer as it did not include any concessions regarding Iran’s nuclear program.

There was more news emanating from the Middle East in late April. The United Arab Emirates (U.A.E.) announced that it will leave the Organization of the Organization of the Petroleum Exporting Countries (OPEC) amid the ongoing tensions in the Gulf region. The U.A.E., the oil cartel’s third-largest producer, is able to avoid the blockade in the strait by rerouting about half of its oil exports across the country. Its withdrawal from OPEC will enable the U.A.E. to increase its output and be less exposed to the impact of the blockade. In statement announcing the withdrawal, U.A.E. officials said, “While near-term volatility, including disruptions in the Arabian Gulf and the Strait of Hormuz, continues to affect supply dynamics, underlying trends point to sustained growth in global energy demand over the medium to long term.”

Elsewhere, Péter Magyar defeated 16-year incumbent Viktor Orbán in Hungary’s presidential election on April 12. In his concession speech, Orbán noted that he had congratulated Magyar on his victory but indicated that that he would remain politically active. ”What today means for our homeland, we do not know. Time will tell. In any case, we will serve our homeland even in opposition.

Economic data

U.S.

Rising energy prices have fueled inflation in the U.S. The Department of Labor reported that the consumer-price index (CPI) jumped 0.9% in March as prices for fuel oil and gasoline surged 30.7% and 21.2%, respectively, during the month, while utility gas service costs fell 0.9%. Prices for fuel oil and gasoline recorded gains of 44.2% and 18.9%, respectively, over the previous 12-month period. Core inflation, as measured by the CPI for all items less food and energy, rose 2.6% year-over-year in March, an uptick from the 2.5% increase in February and slightly below expectations. Costs for transportation services and medical care services were up 4.1% and 3.7%, respectively, over the previous 12-month period, while prices for used cars and trucks decreased 3.2%.

According to the advance estimate from the Department of Commerce, U.S. gross domestic product (GDP) grew at an annual rate of 2.0% for the first quarter of 2026—up sharply from the 0.7% rise in the fourth quarter of 2025, but below expectations. The increase in GDP for the quarter was attributable primarily to upturns in nonresidential fixed investment (purchases of equipment and software, and nonresidential structures), exports, and federal government spending. Conversely, residential fixed investment (purchases of private residential structures and residential equipment that property owners use for rentals) declined during the quarter.

U.K.

According to the Office for National Statistics (ONS), inflation in the U.K., as measured by the CPI, rose 0.7% in March, exceeding the 0.4% increase in February. The upturn in inflation for the month was attributable mainly to substantially higher transportation costs. Prices for education and furniture and household goods were virtually flat. The CPI advanced at an annual rate of 3.3% in March, up from the 3.0% year-over-year rise in February. Housing and household services, and education posted the largest price gains for the month, while costs for clothing and footwear, and furniture and household goods declined.3

The ONS also announced that U.K. GDP was up 0.5% for the three-month period ending February 28 (the most recent reporting period), slightly higher than the 0.3% the growth rate for the three-month period ending January 31. Output in the production and services sectors increased 1.2% and 0.5%, respectively, for the period, while the construction sector output fell 2.0%.4

Eurozone

Eurostat pegged inflation for the eurozone at 3.0% for the 12-month period ending in April, higher than the 2.6% annual increase in March. Energy prices surged 10.9% year-over year in April due to the ongoing blockade in the Strait of Hormuz, affecting a significant amount of global oil capacity, and costs for unprocessed food rose 4.7% compared to the same period in 2025.5

According to Eurostat’s second estimate, eurozone GDP edged up 0.1% in the first quarter of 2026—down marginally from the 0.2% growth rate for the fourth quarter of last year. The economies of Finland, Hungary, Estonia, and Spain were the strongest performers for the first quarter, expanding 0.9%, 0.8%, 0.6%, and 0.6%, respectively. In contrast, GDP for Ireland and Lithuania contracted by corresponding margins of 2.0% and 0.4% during the quarter.6

SEI’s view

The U.S.-Israel-Iran conflict has entered its third month, and global central banks remain in a precarious position. Headline inflation is beginning to reflect the impact of higher oil prices, with motorists increasingly feeling “pain at the pump.” It now appears that Kevin Warsh will soon be confirmed as the next Federal Reserve (Fed) chair. At his final news conference, current Fed Chair Jerome Powell confirmed that, when his term expires in mid-May, he will remain on as a governor—the first chair to take this step since Marriner Eccles in 1948. Powell has cited legal challenges and growing questions around Fed independence as key factors behind his decision. Warsh has been vocal about his preference for a lower federal funds rate, although his ability to build consensus across the Federal Open Market Committee (FOMC) remains an open question.

Given the Fed’s dual mandate of supporting maximum employment and stable prices, we view outright rate hikes as unlikely due to their potentially negative impact on the economy and, ultimately, the labor market. Other global monetary authorities, such as the European Central Bank, are not officially tasked with dual mandates; therefore, they are more likely to focus heavily on price stability, making rate hikes in these regions more conceivable. Nevertheless, we expect global central banks to follow the Fed’s lead to some degree, as major deviations from the Fed’s rate path could destabilize other regions’ foreign exchange rates and capital markets.

SEI continues to expect that the Fed will remain on hold in the near term. Elsewhere, stagflation risks remain elevated, particularly in energy-vulnerable regions such as the U.K. and Europe, where stubborn inflation pressures intersect with sluggish economic growth. We continue to view these regions as the most susceptible to further near-term monetary policy tightening should the conflict prove to be prolonged and energy prices remain elevated.

We remain constructive in our outlook for equities given our current views, including the continued resilience of the economy and corporate earnings. Our strongest preference remains active management due to the fluid situation in the Middle East and higher levels of stock-level dispersion. A value-oriented approach is a particular emphasis, and we expect continued outperformance for the remainder of the year. In addition, we still find emerging markets particularly attractive based on valuations and overall leverage to what we see as a still-growing global economy. Meanwhile, the current tensions raise the most concerns in Europe given the potential for an outsized economic impact from rising energy costs.

Credit markets have continued to digest private credit concerns as software companies became the latest “cockroaches” to emerge. Spreads in this sector widened as the future of software in an artificial intelligence (AI)-enabled world was called into question. The gating of a few high-profile, retail private credit funds also grabbed headlines during the quarter as investors rushed for the exits. While we believe that private credit is due for correction, we are confident that this will be relatively isolated. We simply do not see systemic contagion in this situation and no reflection of the leverage and breadth witnessed in the global financial crisis of the late 2000s. Therefore, while we retain our defensive posture in credit markets, we are eager to take advantage of opportunities presented by this broader spread-widening.

GLOSSARY AND INDEX DEFINITIONS

For financial term and index definitions, please see: seic.com/ent/imu-communications-financial-glossary

IMPORTANT INFORMATION

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated.

This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Not all strategies discussed may be available for your investment.

Information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

For professional clients only. Not suitable for retail distribution.