The Rates Ruckus

We’ve seen a steep rise in rates around the world since the second half of 2020, when promising vaccine results spurred a more optimistic view of the global economic trajectory. The accelerating climb in U.S. Treasury yields since mid-February along with another recent bout of dysfunction in the U.S. repurchase (repo) market—an important source of short-term U.S. dollar funding for banks and other entities—have caused an uptick in market volatility and risk aversion.

The Treasury market selloff has important implications (rates and prices have an inverse relationship, so prices fall when rates rise). One is that interest rates play a central role in valuing financial assets, and higher rates decrease the current value of future cash flows, all else equal, which presents a notable risk to more speculative growth stocks. These stocks are expensive compared to the rest of the equity market (as measured, for example, by the price-to-earnings ratio). This means investors will need more time to recover their purchase costs—via future-year company earnings—while rising rates offer investors an increasingly appealing return from lower-risk alternatives. Another potential consequence is that there may be less pressure for some investors to “reach for yield” as yields on Treasurys rise, which could translate to marginally weaker support for riskier assets.

Interest rates have increased as a result of improving growth and rising inflation expectations, both of which have gotten a boost from recent economic reports and leading indicators. Manufacturing has continued to experience robust growth globally with costs increasing at rapid rates. In some of the few regions where the services sector has started to exhibit a strong recovery, cost increases have reached decade-plus highs1.

Taking a high-level perspective

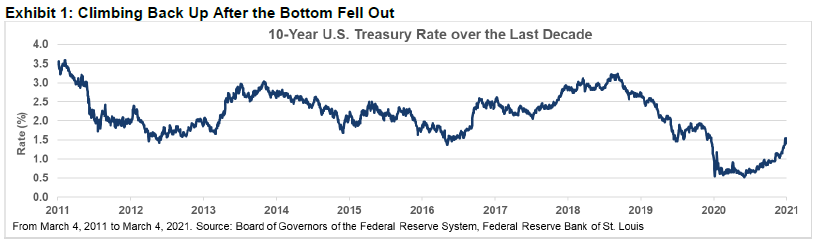

Aside from the flight-to-safety rally that drove Treasury rates to all-time lows early last year, the 10-year U.S. Treasury rate has spent the last decade between 1.5% and 3.0%, with limited isolated exceptions (Exhibit 1). It has only recently returned to the bottom end of its pre-COVID-19 historical range.

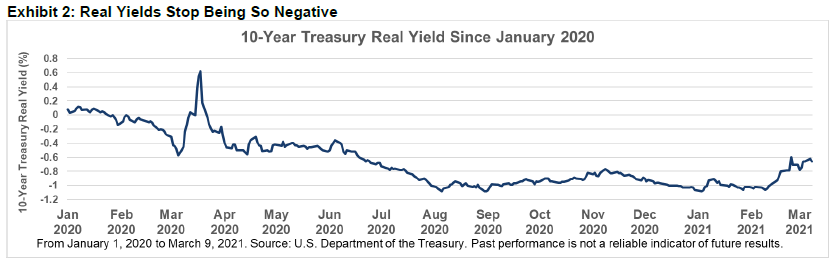

A steepening yield curve (that is, when longer-term yields increase relative to shorter-term yields) is a normal feature of recoveries. While recent steepening has been abrupt, it’s not unprecedented—and suggests a solid economic recovery from the COVID-19 crisis. Furthermore, real (inflation-adjusted) yields have risen, but they have done so from unusually negative levels (Exhibit 2).

The move in rates could eventually cause aftershocks in credit markets. Thus far, however, spreads (that is, the additional yield over Treasurys associated with credit risk) and other measures of financial stress have remained well-behaved.

What are the risks?

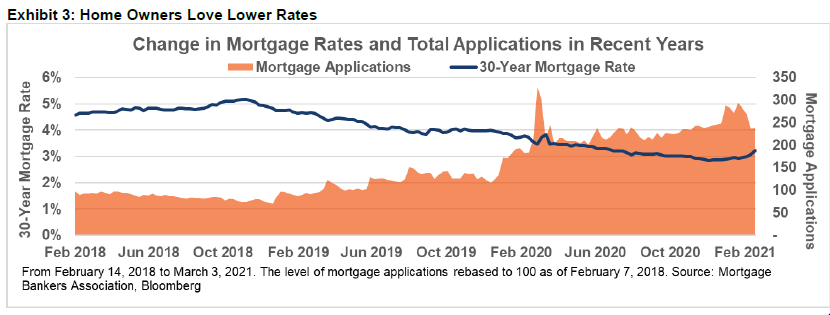

Rising Treasury rates will impact the real economy—mortgage activity, for example, is sensitive to rate changes—but demand for homes is expected to remain robust. However, if rates get too high, they could negatively impact purchase and refinancing activity, which could have adverse repercussions for other areas of the economy.

The 30-year fixed-rate mortgage has historically averaged roughly 170 basis points (bps) more than the 10-year Treasury rate (although this spread can spend months closer to 200 bps when rates fall quickly and remain depressed, as was the case last year). A 10-year Treasury yield around 1.5% would not equate to a significant increase in borrowing costs on most new or refinanced mortgages compared to the historic low rates that were on offer in 2020—but another meaningful move higher could start to cause some stress, especially if it unfolds abruptly.

Will fiscal and monetary policymakers overshoot in their efforts to support the economy?

The U.S. federal government is planning another fiscal expansion of nearly $2 trillion, and the federal deficit (as a share of gross domestic product, or GDP) was already at levels not seen since World War II. There are reasonable arguments on both sides of the debate over the latest round of planned expenditures, but there’s no doubt that such a drastic increase in spending meaningfully increases the risks of higher inflation and rising expectations for inflation.

Thus far, the U.S. Federal Reserve (Fed) has kept its promise to keep rates low and its overall monetary policy accommodative until the labor market and inflation hit levels historically associated with stronger growth. The U.S. economy is still approximately 11 million jobs short of where it would have likely been if not for COVID-19, so the Fed’s full-employment target could take some time to attain2.

Meanwhile, we’re clearly seeing signs of higher inflation. If this persists past the expected year-over-year effects over the next several months (growth can be expected to appear elevated as we measure against the economic-lockdown conditions that defined the beginning of the COVID-19 crisis), Fed dovishness (that is, when its monetary policy is oriented toward supporting shorter-term economic growth) could also risk pushing inflation expectations higher.

It remains to be seen whether or when the Fed would consider adjusting its current approach by selectively targeting certain points of the yield curve. So far, that doesn’t appear to be on the table.

Another set of risks that could influence inflation expectations upward is the recent decision by OPEC+ (the Organization of the Petroleum Exporting Countries, led by Saudi Arabia—plus Russia) to keep oil output tight and the pricing pressures we’ve seen in many commodities over much of the past year’s recovery.

SEI’s view

So far, rate dynamics have been fairly typical of past recovery phases, and we expect they will remain so as we transition to an economic expansion phase. Historically, rates markets periodically adjust their outlook—sometimes abruptly, which can cause bouts of indigestion for risk assets.

We believe that investors should take comfort in the relative regularity of this recovery, but we also know there’s no denying that certain features of this cycle are unusual. The economic effects of COVID-19 are more akin to a natural disaster scenario, when recoveries tend to be sharper and swifter than a typical business cycle. Fiscal measures have also been far more forceful, and the Fed has been at least as dovish, than in past cycles.

For these reasons, we have remained attentive to the risk of eventually overshooting to unsustainably high growth levels and the market dislocations that such a sharp expansion could produce.

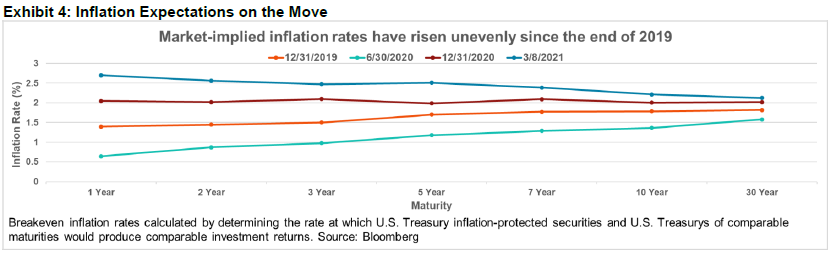

At this stage, the Treasury market has implied stronger growth and faster inflation over an intermediate-term horizon—but it has not pointed to run away or permanently higher inflation (Exhibit 4). Given these unusual developments, however, it is important to understand that the investment experience could be bumpier than usual at times.

The bottom line is that the bond market has quickly caught up to our “reflation” view of faster growth and higher inflation as sizeable and coordinated U.S. fiscal and monetary policies helped accelerate the progression toward a more normal, pre-COVID-19 environment. Generally, inflation-sensitive positioning, value factor exposures, and overweights to sectors like financials have done well in the year-to-date environment, while high-flying growth and stay-at-home names have struggled.

Glossary of Financial Terms

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Price-to-earnings ratio: The price-to-earnings ratio is the ratio of a company's share price to its earnings (typically trailing over the prior 12 months or projected over the next 12 months), which can be used to help determine whether a stock is undervalued or overvalued.

Repurchase (repo) market: The repo market is where borrowers who need short-term cash trade high-quality securities with lenders. Borrowers agree to buy back their securities (typically Treasury instruments) from lenders, usually on the next day. Repo market participants typically consist of banks, money market funds and other large financial institutions.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to "institutional investors" pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to "relevant persons" pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.