Monthly Market Commentary: Stocks begin 2025 on a positive note.

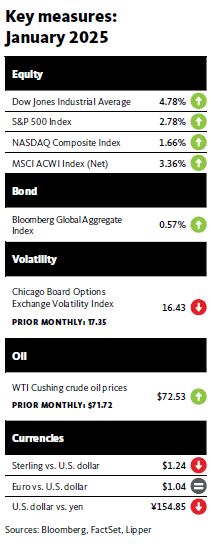

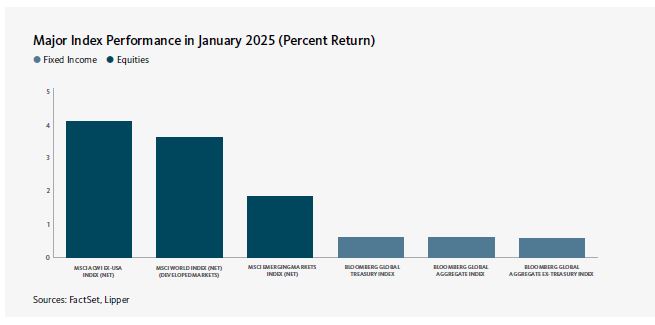

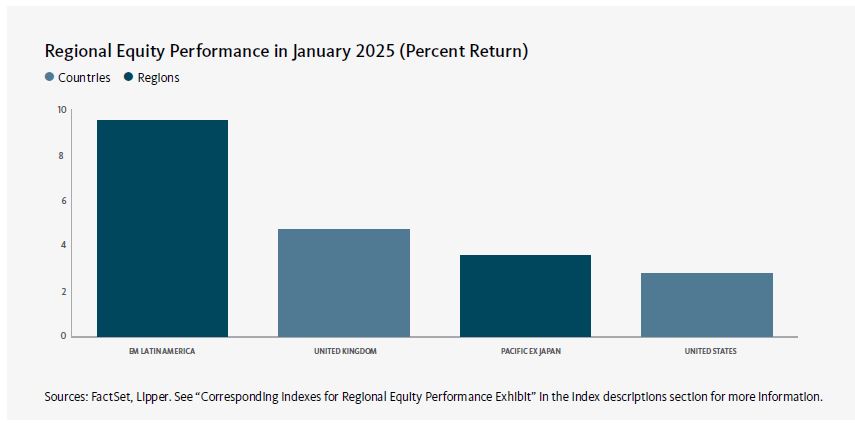

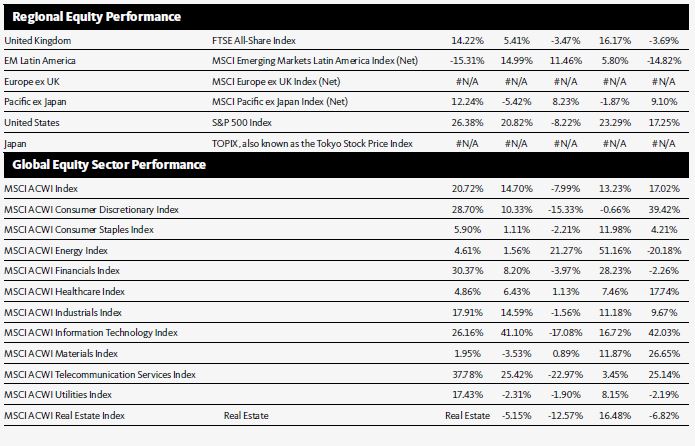

Global equity markets, as measured by the MSCI ACWI Index, garnered positive returns in January, as investors’ confidence was buoyed by generally favorable economic data and upbeat corporate earnings news. However, stocks fell sharply on the last day of the month after the administration of U.S. President Donald Trump announced the assessment of tariffs on imported goods from Canada, Mexico, and China. Developed markets outperformed their emerging-market counterparts for the month. Europe was the strongest-performing region within the developed markets in January, boosted by notable upturns in Sweden, Germany, and Switzerland. Conversely, the Far East posted a much smaller positive return and was the primary market laggard due to weakness in Hong Kong and New Zealand. Eastern Europe led the emerging markets, benefiting mainly from strength in Poland and the Czech Republic. The Association of Southeast Asian Nations (ASEAN) was the weakest emerging-market performer attributable to downturns in the Philippines and Malaysia.

On January 31, President Trump initiated a multi-front trade war with the announced implementation of a 25% across-the-board tariff on Mexico, a 25% tariff on Canada (with an exception for energy, which faces a 10% duty), and a 10% tariff on imports from China. However, on February 3, a day before the tariffs were scheduled to take effect, the Trump administration reached agreements with Canada and Mexico to delay the levies for 30 days after Mexico agreed to send 10,000 troops to the border to combat the flow of fentanyl into the U.S., and Canada pledged to appoint a fentanyl czar, list cartels as terrorists, and launch a joint strike force with the U.S. to combat organised crime, fentanyl trafficking, and money laundering. Nonetheless, the ongoing tariff dispute is volatile and in flux.

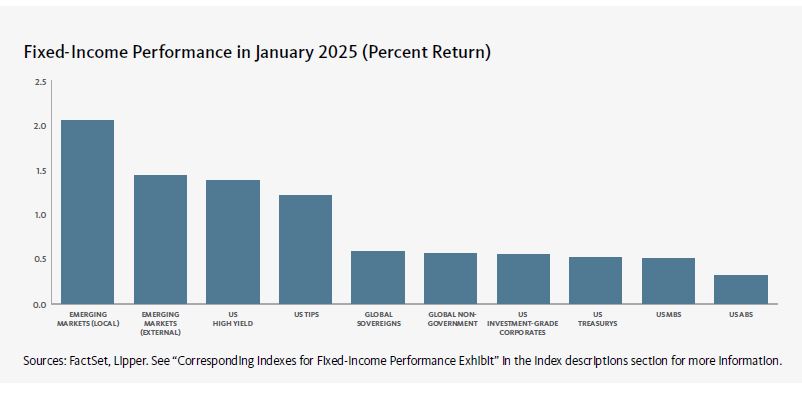

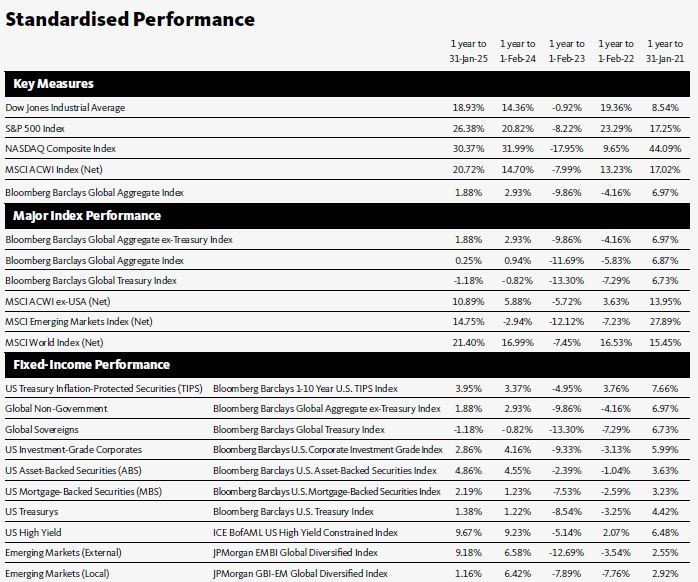

Global fixed-income assets, as measured by the Bloomberg Global Aggregate Bond Index, gained 0.6% in January. High-yield bonds were the strongest performers within the U.S. fixed-income market, followed by investment grade corporate bonds, mortgage-backed securities (MBS), and U.S. Treasurys. There was little movement in Treasury yields during the month. Yields on 2- and 5-year Treasury notes dipped by corresponding margins of 0.03% and 0.02% to 4.22% and 4.36%, while the 3- and 10-year yields were flat, ending the month at 4.27% and 4.58%, respectively.2 The spread between 10- and 2-year notes widened by 0.03% to +0.36% over the month, as the yield curve remained positively sloped (longer-term yields exceeded shorter-term yields). A positively sloped yield curve generally indicates that the economy is expected to grow in the future.

Global commodity prices, as represented by the Bloomberg Commodity Index, rose 4.0% in January. The West Texas Intermediate (WTI) and Brent crude oil prices posted corresponding increases of 1.1% and 1.4%, to $72.53 and $75.67, respectively, over the month due to concerns about the imposition of tariffs by the U.S. on oil imported from Canada and Mexico. Uncertainty regarding the tariffs led to a 7.3% surge in the gold spot price as investors sought safe-haven assets. The New York Mercantile Exchange (NYMEX) natural gas price fell 1.6% during the month due to forecasts for relatively warmer weather in the U.S. for the remainder of winter. Wheat prices were up 1.5% in January, bolstered by increased demand for exports from the U.S.

On the geopolitical front, Israel and Hamas agreed to a pause in their 15-month war, effective on January 19. The plan is being implemented in three phases, beginning with a ceasefire and the exchange of some Israeli hostages held in Gaza by Hamas for Palestinian prisoners detained by the Israeli government. The two sides then will try to reach an agreement for a permanent end to the conflict. Israel released 90 Palestinians on January 19, followed by another 200 six days later. In response, Hamas freed three female civilians from Israel and four female Israeli soldiers.

Economic data

U.S.

The Department of Labor announced that the consumer-price index (CPI) advanced 0.4% in December, slightly higher than the 0.3% increase in November. The uptick in inflation was not broad-based, however, as energy costs comprised more than 40% of the increase, rising 2.6% during the month, as gasoline and fuel oil prices each surged 4.4%. The 2.9% year-overyear advance in the index was up from the 2.7% annual rise in November and was in line with expectations. Costs for transportation services and housing climbed 7.3% and 4.6%, respectively, over the previous 12-month period, while energy and commodity prices each fell 0.5%. Core inflation, as measured by the CPI for all items less food and energy, rose at a lower-than expected rate of 3.2% year-over-year in December, down marginally from the 3.3% annual increase in November.

According to the initial estimate from the Department of Commerce, U.S. gross domestic product (GDP) grew at an annualised rate of 2.3% in the fourth quarter of 2024—down from the 3.1% increase in the third quarter. The U.S. economy expanded by 2.5% for the 2024 calendar year, lagging the 3.2% annual gain in 2023. The largest contributors to GDP growth for the fourth quarter included consumer spending and federal government spending. This was partially offset by a decline in nonresidential fixed investment (purchases of both nonresidential structures and equipment and software). The government attributed the quarter-over-quarter decline in the GDP growth rate to downturns in nonresidential fixed investment and exports.

U.K.

The Office for National Statistics (ONS) reported that inflation in the U.K., as measured by the CPI, increased 0.3% in December, slightly higher than the 0.1% rise in November. The CPI advanced at an annual rate of 2.5% in December, down marginally from the 2.6% rise for the previous month. Costs for communication, health care, and alcohol and tobacco posted corresponding increases of 6.1%, 5.6%, and 5.3%, year-over-year, while prices for transportation and furniture and household goods declined 0.6% and 0.3%, respectively, over the previous 12-month period. Core inflation, which excludes volatile food, energy, and alcohol and tobacco prices, rose by an annual rate of 3.2% in December, down from the 3.5% year-over-year increase in November.

The ONS also announced that U.K. GDP growth edged up 0.1% in November, and was flat over previous three months (the most recent reporting periods). The marginal rise in GDP for November was an improvement from the 0.1% dip in October. Output in the construction sector rose 0.2% for the three month period ending November 30, while growth in the services sector was flat, and production output fell 0.7%.

Eurozone

Eurostat pegged the inflation rate for the eurozone at 2.5% for the 12-month period ending in January, marginally higher than the 2.4% annual upturn in December. Costs in the services sector rose at an annual rate of 3.9%, unchanged from the increase in December. Prices for food, alcohol and tobacco increased 2.3% year-over-year in January, down from the 2.6% annual rate for the previous month. Core inflation, which excludes volatile energy and food prices, increased at an annual rate of 2.7% for the fifth consecutive month in January.

Eurostat also reported that eurozone GDP growth rate was flat in the fourth quarter of 2024, weakening from the 0.4% increase in the third quarter. The eurozone economy expanded by 0.7% year-over-year—down modestly from the 0.9% annual growth rate for the previous quarter. The economies of Portugal, Lithuania, and Spain were the strongest performers for the fourth quarter, growing 1.5%, 0.9%, and 0.8%, respectively. In contrast, GDP in Ireland declined 1.3% during the quarter.

SEI’s view

The Trump administration’s possible imposition of tariffs on America’s three largest trading partners has the potential to increase prices and lower economic growth. The precise impact is unclear, since we do not know how aggressive the tariffs will be or how long they will stay in place. We do know that tariffs on goods from Colombia were short-lived and that this president loves to make deals. We think that the Trump administration’s proposed tariffs could send Mexico and Canada into a moderate recession in the months ahead given their high dependence on the U.S. market. The U.S. could sustain a sharp deceleration of growth and may even experience a pullback in industrial output given the extent of economic integration with its two major trading partners. A broadening of the trade war to include Europe and Asia would further depress economic growth, but on a global scale. In the near-term, supply-chain disruptions and retaliatory actions could increase U.S. inflation beyond 3%. Canada’s economy, already struggling before the imposition of tariffs, should see a further slowing of its inflation rate. Monetary policy across the developed world was already diverging, with interest rates falling more in Canada and the Eurozone than in the U.S. An expanding trade war would exacerbate this trend. Monetary policy divergence also implies a further strengthening of the U.S. dollar.

We see too many potential outcomes leading to a reacceleration in inflation and higher long-term interest rates. The bond market seems to share our concerns, as the 10-year U.S. Treasury yield rose 93 basis points (0.93%) since the Fed pivoted to reducing interest rates with a surprising 50-basis-point cut in mid-September to the end of January. The yield on the 10-year U.S. Treasury is our guide for 2025. We will become concerned about equity markets once the yield reaches 5%, as tighter financial conditions may begin to weigh on growth prospects.

We maintain our strategic recommendations for investors to stay diversified globally and focus on profitable companies with strong earnings momentum trading at reasonable prices. Given our views on the likelihood of higher interest rates and heightened volatility, we continue to lean into value and active management across our equity strategies. We favor sectors such as financials, industrials, and staples.

Within fixed-income markets, we remain cautious on interest rates and sanguine on credit. We believe the Fed is still biased toward lower rates (although the central bank left the federal-funds rate unchanged in January) despite core consumer price index and gross domestic product readings both above 3%. In addition, the reality of tariffs and immigration reforms may add additional fuel to the inflation fire. Consequently, we see headwinds for fixed income returns. On a more positive note, while credit spreads have limited room to tighten, absolute yields remain attractive, defaults remain low, and maturities have been extended.

Glossary of Financial Terms

Yield is the income returned on an investment, such as the interest received from holding a security. The yield is usually expressed as an annual percentage rate based on the investment’s cost, current market value, or face value.

Yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (are (which is used to assess the risk of default of companies or countries). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates that short- and long-term yields are closer together.

Monetary policy refers to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Index definitions

All indexes are quoted in gross performance unless otherwise indicated.

The MSCI ACWI Index is a market capitalization-weighted index that tracks the performance of over 2,000 companies, and is representative of the market structure of 48 developed and emerging-market countries in North and South America, Europe, Africa, and the Pacific Rim. The index is calculated with net dividends reinvested in U.S. dollars.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

The Bloomberg Global Aggregate Bond Index is a market capitalization-weighted index that tracks the performance of investment grade (rated BBB- or higher by S&P Global Ratings/Fitch Ratings or Baa3 or higher by Moody’s Investors Service) fixed-income securities denominated in 13 currencies. The index reflects reinvestment of all distributions and changes in market prices.

The S&P US Mortgage Backed Securities Index tracks the performance of U.S. dollar-denominated, fixed-rate and adjustable-rate/hybrid mortgage pass-through securities issued by Ginnie Mae (GNMA), Fannie Mae (FNMA) and Freddie Mac (FHLMC).

The ICE BofA U.S. Corporate Index includes publicly issued, fixed-rate, nonconvertible investment-grade (rated BBB- or higher by S&P Global Ratings and Fitch Ratings or Baa3 or higher by Moody’s Investors Service) dollar-denominated, U.S. Securities and Exchange (SEC)-registered corporate debt having at least one year to maturity.

The ICE BofA U.S. High Yield Constrained Index is a market value-weighted index of all domestic and Yankee high-yield bonds, including deferred interest bonds and payment-in-kind securities, with maturities of one year or more and a credit rating of BB+ or lower by S&P Global Ratings and Fitch Ratings or Ba1 or lower by Moody’s Investors Service, but are not in default.

The ICE BofA U.S. Treasury Index tracks the performance of the direct sovereign debt of the U. S. government.

The Bloomberg Commodity Total Return Index comprises futures contracts and tracks the performance of a fully collateralized investment in the index. This combines the returns of the index with the returns on cash collateral invested in 13-week (three-month) U.S. Treasury bills.

Consumer-price indexes measure changes in the price level of a weighted-average market basket of consumer goods and services purchased by households. A consumer price index is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected periodically.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated.

This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Not all strategies discussed may be available for your investment.

Information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

For professional clients only. Not suitable for retail distribution.