Monthly Market Commentary: Investors Look Forward to Looser Lockdowns

Global financial markets continued their sharp rallies in May, albeit short of their remarkable April rebounds. The “risk-on” sentiment came amid a push by local governments to slowly reverse lockdowns of non-essential economic activity; the promising news of progress made in the race to develop COVID-19 vaccines; and the sustained extraordinary support of central banks.

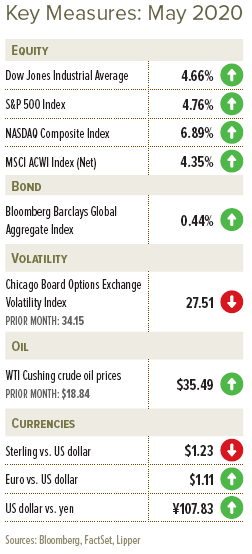

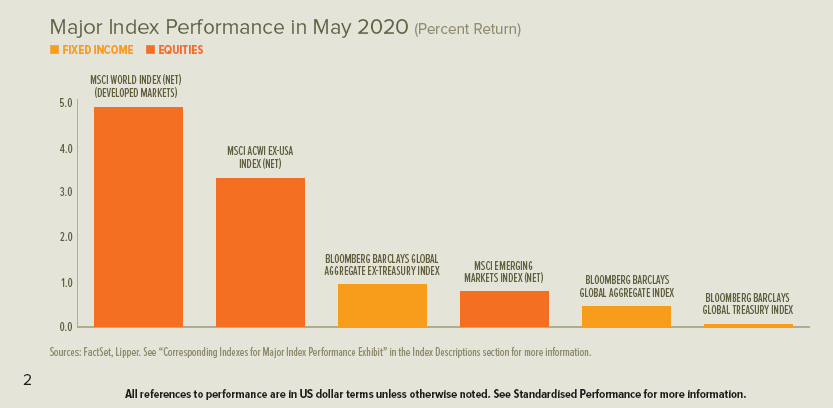

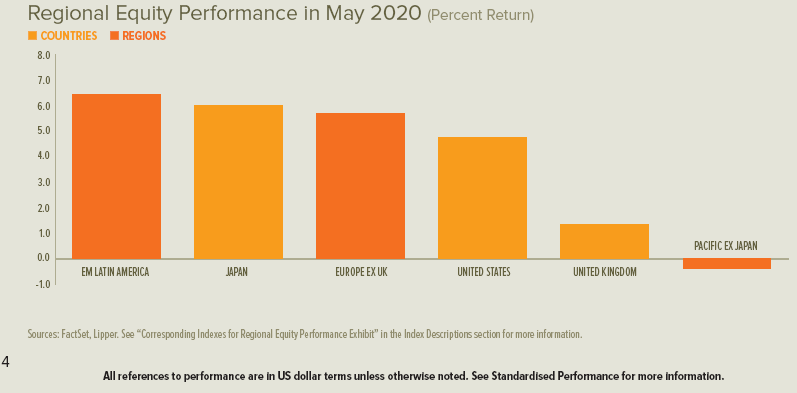

Equities around much of the world experienced a choppy first half of May that ultimately gave way to a strong second half for the month. However, mainland Chinese and Hong Kong shares were outliers; both came under pressure as the month progressed, with the island territory finishing the period with a steep loss. European and US shares generated solid monthly performance, while UK shares delivered more subdued gains.

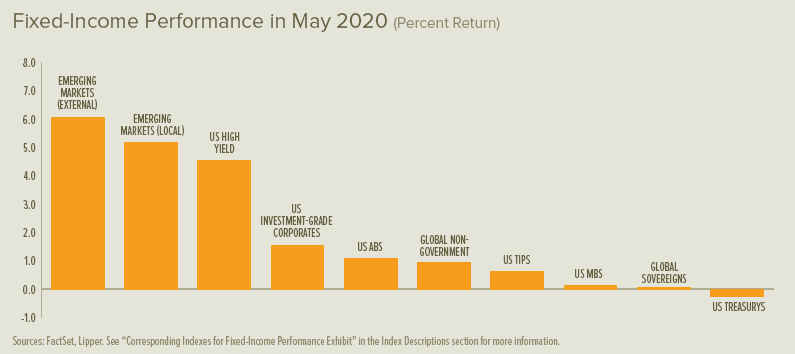

Government-bond rates followed divergent paths from country to country. They mostly declined for UK gilts, yet increased for those with the longest maturities, while they increased across all maturities for eurozone government-bonds. As for US Treasurys, short- and long-term rates increased as intermediate-term rates declined for the month.

The UK COVID-19-related death toll eclipsed that of Italy in early May, reaching the highest number of losses in Europe (although Italy lost a greater percentage of its smaller population). UK Chancellor of the Exchequer Rishi Sunak announced his intention to extend the government’s mortgage-payment holiday beyond June as its initial three-month timeframe approached. As of mid-May, UK banks had granted these repayment holiday terms to 1.7 million homeowners1.

Italy provided reason to celebrate halfway through the month as its number of new COVID-19 cases per day fell below 100 for the first time since March. The peninsular nation announced plans to begin reopening borders in early June. Prime Minister Giuseppe Conte proposed a €55 billion relief package intended to freeze corporate taxes for many businesses; provide forgivable grants of up to €40,000 for small businesses and emergency incomes of up to €800 for struggling families; extended unemployment payments; and offer funding for healthcare, tourism, research and agriculture, among others initiatives. The Italian government’s announcement preceded the mid-May proposal by the European Commission for nearly €2 trillion across the EU, with €750 billion devoted to recovery efforts and another €1.1 trillion to budgets over the next seven years.

In the US, the total recorded number of COVID-19-related deaths surpassed 100,000 in late May—out of about 350,000 total worldwide. President Donald Trump’s administration imposed travel restrictions on Brazil amid the South American nation’s struggle to contain the outbreak; the US federal government also prolonged its mandate for land-border closures with Canada and Mexico by one month, now effective through 22 June. State-by-state responses continued to vary widely, with some local governments facing challenges to the legality of their orders: Wisconsin’s state supreme court overturned the governor’s stay-at-home order in mid-May; the US Supreme Court (the nation’s highest court) rejected a California church’s challenge to the legality of placing restrictions on gathering in places of worship—thereby validating California’s state government to enforce such restrictions.

US legislators continued to explore ways to improve the Paycheck Protection Program—a government loan designed to incentivise small businesses to keep workers on the payroll—legislation passed the US Congress in early June that would extend the period during which companies can spend loan proceeds and remain eligible for loan forgiveness, as well as allow a lower minimum share of loan proceeds to go toward covering payroll. Toward the end of May, the House of Representatives also passed an additional $3 trillion in COVID-19 relief funds, but the legislation was held up in the Senate with unclear prospects for approval.

The National People’s Congress in China concluded the month with its approval of a resolution to impose new national-security laws on Hong Kong amid ongoing anti-Beijing protests, marking a significant dilution of the “one country, two systems” governance ethos that has defined the relationship since the UK’s handoff of Hong Kong to China in 1997.

Several governments around the world condemned this development and began to explore concrete responses. UK Prime Minister Boris Johnson said Britain was considering a path to citizenship and relocation for British Nationals (Overseas) (a class of British nationality extended to Hong Kong residents prior to the 1997 handover). Meanwhile, the US began examining Hong Kong’s special territorial exemptions and evaluating multiple avenues for putting economic pressure on China—including sanctioning the mainland Chinese financial sector and imposing limitations on technology sharing by adding dozens of Chinese entities to trade blacklists.

The increasingly tense US-China relationship was further stressed in May by a US push for more transparency in the ownership of US-listed Chinese companies and the US government’s barring of certain Chinese holdings from its retirement plans. Canada’s relationship with China was also strained during the month after a Canadian judge ruled in favour of a US petition to extradite a Chinese telecommunications executive. China, for its part, imposed an 80% tariff on all barley imported from Australia over the next five years in an apparent response to the Australian government’s call for an independent inquiry into the origins of COVID-19.

Economic Data

Sharp contractions in manufacturing and services conditions appeared to slow across the UK, eurozone and US during May, but remained far from returning to growth. Preliminary reports showed services activity in the US was moderating quicker than in the UK and eurozone.

- The UK economy shrank by 5.8% during March, representing the largest monthly decline in more than 20 years of UK gross domestic product (GDP) measurements2. Economic activity contracted by 2% over the first quarter of 2020. The UK claimant count (which measures the number of people claiming unemployment benefits) jumped from 3.5% in March to 5.8% in April. Retail sales in the UK fell in April by 18.1% from the prior month and by 22.6% from a year earlier.

- The eurozone contracted by 3.8% during the first quarter and 3.2% over the one-year period. Construction output dropped 14.2% in March after slipping just 0.5% in February. Loans to non-financial corporations climbed by 6.6% in April, following an increase of 5.4% in March, continuing a corporate-credit bounce from February’s ebb.

- US consumer spending fell by 13.6% during April, registering the sharpest one-month decline since the data series began in 19593. New jobless claims for US unemployment benefits declined from more than 3 million per week in early May to about 2 million later in the month; continuing claims fell during the week of 16 May for the first time since COVID-19 lockdowns began in the US. Nearly 15 million US credit card bills went unpaid during April, and more than 8% of US mortgages were in forbearance as of mid-May. US GDP declined by an annualised 5% during the first quarter of 2020, the largest quarterly decline since the final three months of 2008.

Central Banks

- The Bank of England’s (BoE) Monetary Policy Committee held course following its 7 May meeting, keeping the Bank Rate at 0.1% and reiterating a commitment to purchase £200 billion in gilts and investment-grade corporate bonds (at its current pace of buying, this would bring the BoE’s stock of asset purchases to £645 billion by the beginning of July). The central bank’s May policy statement cited data that point to a significant drop in household consumption and plummeting expectations for sales and business investment during the second quarter.

- The European Central Bank (ECB) did not meet to address monetary policy in May following its end-of-April unveiling of a new lending program called the pandemic emergency longer-term refinancing operations, or PELTROs, to help facilitate proper functioning of money markets. Germany’s constitutional court ruled during May that the ECB must produce justification for the legality of its bond-buying programme, which began in 2015, in order to determine whether the Bundesbank could continue to participate.

- The US Federal Open Market Committee held no meeting in May after maintaining its monetary-policy orientation at a late-April meeting. As part of its crisis-period response, the Federal Reserve (Fed) began buying corporate bond exchange-traded funds on 12 May to support secondary-market liquidity. Fed Chair Jerome Powell announced near the end of May that the central bank’s Main Street Lending Program—introduced to support the small-business loan market—would be operational within days.

- The Bank of Japan (BOJ) did not conduct a meeting on monetary policyduring May. At its late-April meeting, the BOJ committed to open-endedpurchases of Japanese government bonds in an effort to keep yields lowand stable, and announced a ramp-up to its purchases of corporate bondsand commercial paper to a target of ¥20 trillion.

SEI’s View

Black swans, once largely presumed a myth because only the white variety was ever observed in nature, have become symbols of events that are exceptionally rare in occurrence and severe in impact. Today we are confronted with a black swan that landed earlier this year in the form of a pandemic.

The sudden and widespread stop in economic activity by government fiat is something that has never before been experienced on such a scale. The ultimate impact on GDP is truly anybody’s guess. The first quarter of 2020 saw an annualised decline of 5% in the US. The second quarter will likely be one for the record books; as of late May, Wall Street economists forecasted a quarter-to-quarter annualised decline exceeding 30%.

National governments have been quick to respond. All central banks are in crisis-fighting mode, having learned valuable lessons during the 2008-to-2009 great financial crisis, re-establishing unconventional bond-buying programmes and creating some new facilities to expand the types of accepted collateral in order to extend cash to companies in need of liquid assets.

The Fed and other leading central banks have moved with an alacrity and forcefulness that we find commendable. But central banks cannot single-handedly support this economic shutdown. In our view, fiscal policy—in the form of direct income support, tax deferrals, loan guarantees, and outright bailouts of industries badly damaged by the halt of economic activity—must be the prime tool used to address this crisis.

The fiscal response is occurring with a speed and decisiveness seldom seen in history. The US Congress passed a series of COVID-19 relief bills that easily topped 10% of GDP. Other developed countries have pursued a similar strategy of massive income support and liquidity injections. Italy, the European epicentre of the virus, will be particularly hard-pressed to do all that is necessary to stabilise its economy; its government debt-to-GDP ratio is already well above that of other major European countries4.

In our view, a financial crisis can be averted in Europe if the ECB backs up the debt. This is now-or-never time for the EU and eurozone. The stronger countries must come to the aid of the weaker, or else face an intensified popular backlash that could threaten the unity of the economic zone.

The onslaught of developments presented by the spread of COVID-19 has forced financial markets to recalibrate prices sharply as expectations about different industries and the overall economy shift quickly. Investors should gain some reassurance, however, from the fact that an earnings recession caused by virus-containment measures is generally only expected to last a couple quarters or so. If market prices are based on a long-term, multi-year expectation, then this fallout should represent a relatively small part of the market’s forward-looking focus.

We are grateful that the chaotic trading in March has eased considerably, thanks to liquidity provided by central banks and fiscal packages offered by governments around the world. Only time will tell whether markets have sufficiently discounted the pain that lies ahead. We have to be cognisant of the fact that earnings estimates will likely come down hard over the next two quarters. These waterfall declines in earnings could still drag equities down with them. It all depends on how willing investors are to look beyond the valley. Markets should prove resilient if there is a common belief that fiscal and monetary responses to the crisis thus far will successfully prop up the global economy.

Right now, as always, we are focused on trying to deliver as diversified a portfolio as possible to all of our investors, regardless of their risk tolerances. We’re considering the known risks inherent to the capital markets as well as the uncertainty that comes with any long-term investing plan, such as the black swan we’ve encountered in 2020.

At SEI, we build and maintain long-term-oriented portfolios by being attuned to evolving correlations, or relationships, between asset classes. We view our strategies as robust and built to handle the kinds of challenges presented in today’s environment.

At a portfolio level, we encourage investors to stay diversified and avoid short-term trading in these volatile markets. If you are a goals-based investor—and your portfolio is aligned with your goals, time horizon and risk tolerance—be patient. Time should be on your side.

You’re seeing a real-life, albeit metaphorical, black swan. Use this experience to become a better, more informed investor. We will continue to monitor economic and financial-market developments and provide our insight to help you achieve that goal.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to do so) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Paycheck Protection Program: The Paycheck Protection Program is a loan offer by the U.S. government’s Small Business Administration (SBA) designed to provide a direct incentive for small businesses to keep their workers on the payroll. SBA will forgive loans if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

Pandemic Emergency Longer-Term Refinancing Operations (PELTROs): PELTROs are a series of longer-term refinancing operations intended by the ECB to ensure sufficient liquidity and smooth money market conditions during the COVID-19 pandemic period. PELTRO operations are planned to be allotted on a near-monthly basis maturing in the third quarter of 2021.

Repo funding: Repo (also known as a repurchase agreement) refers to a type of short-term borrowing for dealers in government securities. Central banks can increase the cash available to commercial banks by repurchasing the government securities that

they own.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.