FAQ: Russian-related holdings and exposure

This FAQ is designed to help provide an update on the current Russia/Ukraine crisis and portfolio exposure to Russian-related securities.

Q. Do I have any exposure to Russian-related securities remaining in my portfolio?

A. In order to ensure that our response is clear, we need to define several terms, including:

- Russian-related securities, as defined by SEI (and aligned with the definitions used by major index providers and other data providers) are:

i) Securities listed on an exchange domiciled in Russia, Ukraine or Belarus;

ii) Securities listed on an exchange outside of these countries but that derive an extensive portion of their business from Russian, Ukrainian or Belorussian operations;

iii) Debt issued by Russian, Ukrainian or Belorussian public or private entities with the exception of Ukrainian hard-currency bonds (U.S. dollar and euro) in our emerging-market debt portfolios. We have lifted the restriction on the purchase of these bonds. This change will permit hard-currency managers Marathon and Stone Harbor and blended debt manager Neuberger Berman to purchase Ukraine hard-currency bonds.

- Russian-related holdings are Russian-related stocks or bonds owned by an SEI Fund, regardless of value.

- Russian-related exposure refers to the value of the Russian-related holdings stated as a percentage of the value of the Fund as a whole.

The value of Russian securities steeply declined in the aftermath of the invasion as the market absorbed domestic and international sanctions against Russia, actions by index providers, and suspension of trading of certain Russian securities.

Any portfolio that had holdings in Russian-related equity securities when the Russian financial markets closed still owns those holdings. However, in terms of exposure, most of those holdings currently have little or no value. If your portfolio includes Russian-related equity securities that are all valued at $0, you have Russian-related holdings but your current exposure is zero. This can be seen clearly in the holdings chart where columns show 0 exposure.

It is important to keep in mind that if and when Russian financial markets reopen, equity securities that are currently valued at zero could rise in price. By regulation, security valuations are required to be based on the fair market value (FMV) of securities, and cannot be based on political views or an intention to avoid exposure to Russian-related securities. Therefore, if the FMV of Russian securities increases, then a portfolio that includes Russian holdings will also see its value rise in tandem. The portfolio’s corresponding exposure to Russia will also increase. In other words, the Russian exposure in the portfolio could increase even though there have been no additional purchases of Russian-related securities.

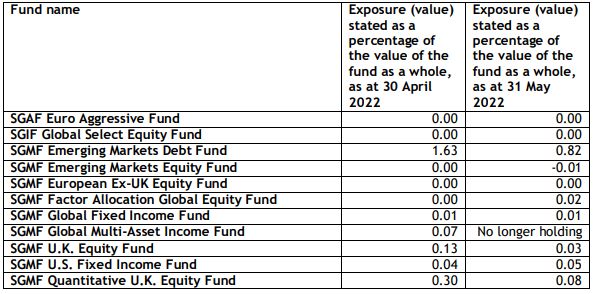

Q. Which SEI Funds have holdings in Russia-related securities and what is the current exposure (value) of those holdings in those portfolios?

A. The chart below highlights exposure at the end of April and end of May. The Funds that had Russian-related equity holdings at the end of February still have them at the end of May. As previously noted, a portfolio holding Russian-related securities that are all valued at $0, still has Russian-related holdings but the current exposure is zero because they have no value. This can be seen clearly in the chart where columns show 0 exposure.

Note: Note: If exposure increased from March to April, this is due to an increase in value of existing holdings and not the purchase of additional securities.

NOTE: The negative exposures are a result of currency forwards that were included in the final calculation.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the ”SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS regulations. Investments in SEI Funds are generally medium to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice. Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document, Summary of UCITS Shareholder rights (which includes a summary of the rights that shareholders of our funds have) and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents. And you should read the terms and conditions contained in the Prospectus (including the risk factors) before making any investment decision.

Important information

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to "institutional investors" pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to "relevant persons" pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This commentary and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.