ESG ratings: What are those all about?

The rise in sustainable investing has invariably brought with it a plethora of data and information, along with a lot of media attention. Much of the data and information about companies used in sustainable investing has historically been self-reported, voluntary, backward looking, non-standardized, and, therefore, inconsistent over time and from one company to the next.

In the 2000s, a cottage industry emerged to help make sense of the growing mountain of data by supplying subscribers with raw data, screens (algorithms designed to exclude selected securities based on predefined criteria), and alerts (instant communications that apprise subscribers of changes to predetermined criteria). Providers each developed their own approach to analyzing and synthesizing the data into scores or ratings, intended to simplify subscribers’ assimilation and use of the vast information. Unfortunately, however, even the best of intentions can lead to unwelcome results. In the case of ESG data vendors, it was the ratings more so than the underlying data that has caused frustration and confusion for investors and companies alike.

Consolidating list of ratings and data providers

Over the years, the ESG data and ratings industry has consolidated into several major providers:

- MSCI

- Sustainalytics (owned by Morningstar)

- Refinitiv (owned by Thomson Reuters)

- ISS ESG

- S&P Global

- Bloomberg

And a few key specialist data providers:

- CDP

- Trucost

- RepRisk

According to a 2022 ESG manager survey by management consultancy Opimas, four of the major providers account for nearly 70% market share—with MSCI at approximately 31%, ISS ESG at 17%, and Sustainalytics and S&P Global each at 10%. This consolidation combined with the surging interest in sustainable investing has given these vendors an increasingly important role in the investment landscape. Even so, a basic internet search reveals in excess of 100 different ESG data vendors in the market today (versus three primary credit-rating agencies).

Expanding list of index funds

Meanwhile, the growth of passive investing has deeply entrenched ratings into the sustainable investing landscape. According to the Index Industry Association, there are more than 50,000 ESG indexes available to investors across asset classes globally.1 A single ratings provider, MSCI, has more than 1,500 such indexes, many of which leverage its ratings for constituent selection. In the U.S., 30% of sustainable funds, and 40% of the assets in them, are passive strategies.2

Providers may:

- Use more or less data to assess a topic.

- Use different data points or indicators to assess a topic.

- Use different ways to measure the same data.

- Use different methods to translate qualitative insights into quantitative data.

- Have different views on which issues are material for a given company or sector.

- Put different weights on factors across companies.

Alphabet soup: Lots of data, lots of funds, few standards

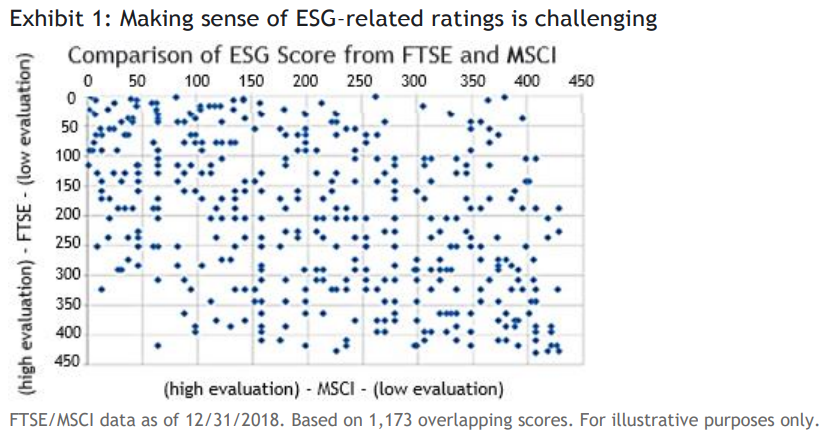

Unfortunately, the state of ESG ratings is only modestly better today than it was five or even 10 years ago. While there is now more data to inform these ratings, that doesn’t necessarily mean that investors have made much headway in their understanding of how ratings are determined. Meanwhile, the level of investor interest in and demand for ESG information has risen. In many cases, transparency about data sources, calculation methods, and aggregation approaches remains elusive (see Exhibit 1).

An effort to make sense of the data and ratings led to seminal work by Florian Berg, Julian Kolbel, and Roberto Rigobon at MIT Sloan called Aggregate Confusion: The Divergence of ESG Ratings (originally published in August 2019 and updated in April 2022). They concluded from their research that the primary differences between ESG rating providers were related to measurement (56%), scope (38%), and weight (6%).

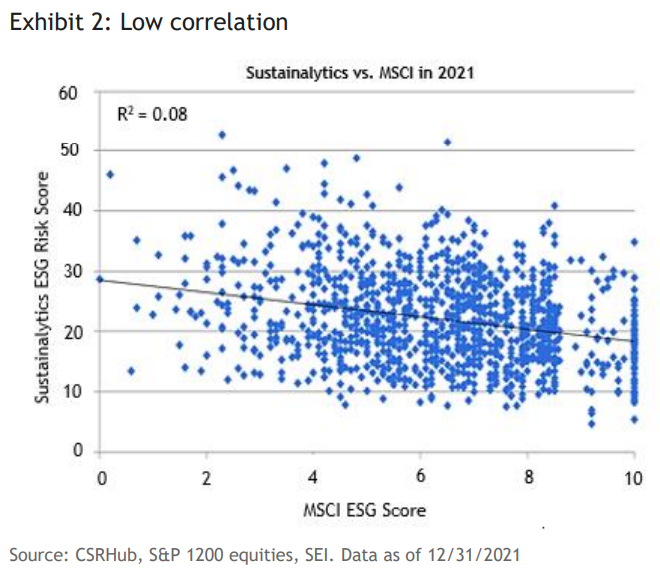

For investors wanting to incorporate ESG considerations into their investment process but unable to independently acquire, process, or synthesize the large volume of ESG data available, the default has been to use ratings provided by vendors. According to the International Organization of Securities Commissions (IOSCO), ESG ratings can be defined as the broad spectrum of ratings, rankings, and scorings that serve the assessment of an entity, an instrument, or an issuer’s exposure to ESG risks and/or opportunities. Unlike credit ratings, with their high degree of consistency and correlation across vendors such as Moody’s and S&P, ESG ratings are low-to-modestly correlated (see Exhibit 2)—leaving users to question the efficacy of ESG ratings, how to choose between them, and how to apply them.

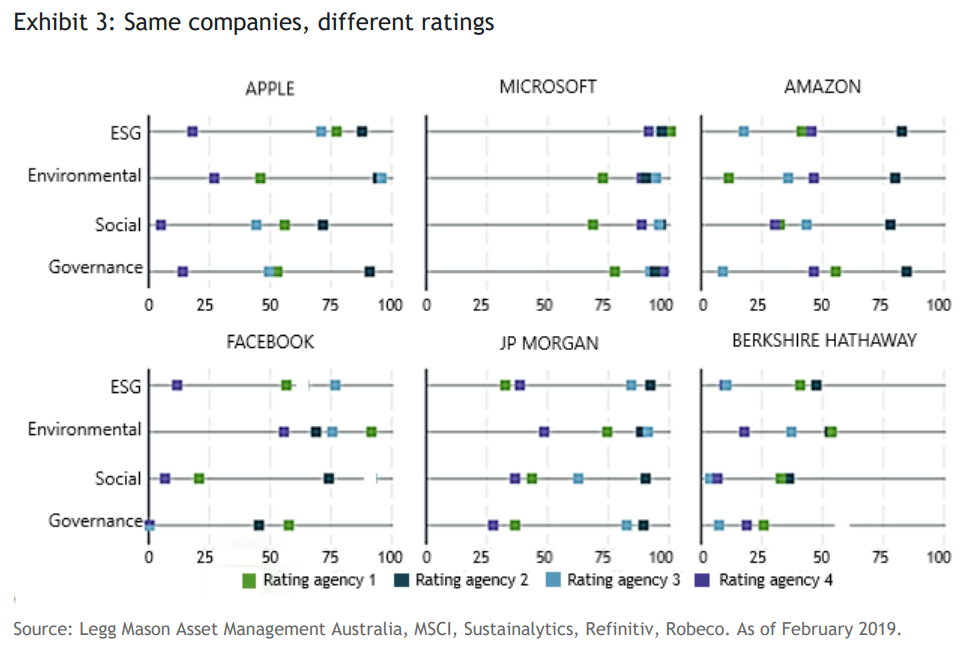

Exhibit 3 provides a more granular example of rating divergences at the company level using FTSE Russell (FTSE) data (while FTSE does not have a market share position as large as Moody’s or S&P, FTSE is a major, well-known provider).

What is an ESG Rating?

Contrary to what many likely believe, an ESG rating is NOT an appraisal of a company’s effect on the world—nor is it a measure of the stakeholders’ non-financial concerns (such as proxy voting or shareholder engagement).

ESG ratings are an assessment of how well a company manages the risks and opportunities associated with environmental, social, and governance issues.

They serve to help investors recognize and manage exposures to ESG-related risks by aggregating and summarizing more granular information and insights. Given that all investment strategies are exposed to such risks, ESG ratings can be an important risk-management tool for any investor.

ESG ratings are based on data that must be sourced and measured.

By “data,” we mean information about companies that is both granular (such as total carbon emissions, recordable injury rates, or board of directors’ gender composition) as well as qualitative (such as talent-development programs or community relations).

Next, the vendors must determine the relevance and materiality of each data set. They may deem social factors as more relevant for assessing software companies, for example, and information about carbon emissions as more important to the assessment of oil and gas companies.

Finally, before deriving a company’s final ESG rating (whether absolute or normalized relative to peers), the vendors must weigh everything (for instance, MSCI applies up to six key indicators to a given industry) and rank/score the degree to which a company manages risks and opportunities associated with ESG issues (relative to other companies within its industry or across industries).

Why do ESG ratings and ESG data matter?

Making investment decisions based on a vendor’s ESG ratings requires adopting that vendor’s view of what, how, and how much to measure different types of ESG data. In many cases, doing so offers efficiency and comparability across strategies and managers—such as the case in passive investing. However, it remains important to understand the distinction between ESG ratings and the data from which they are derived.

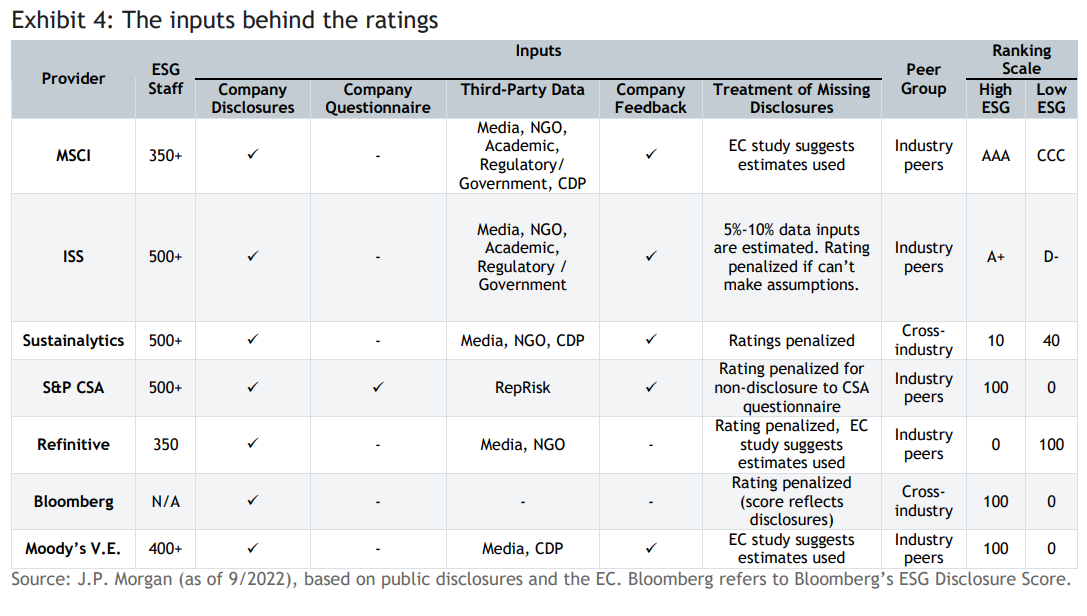

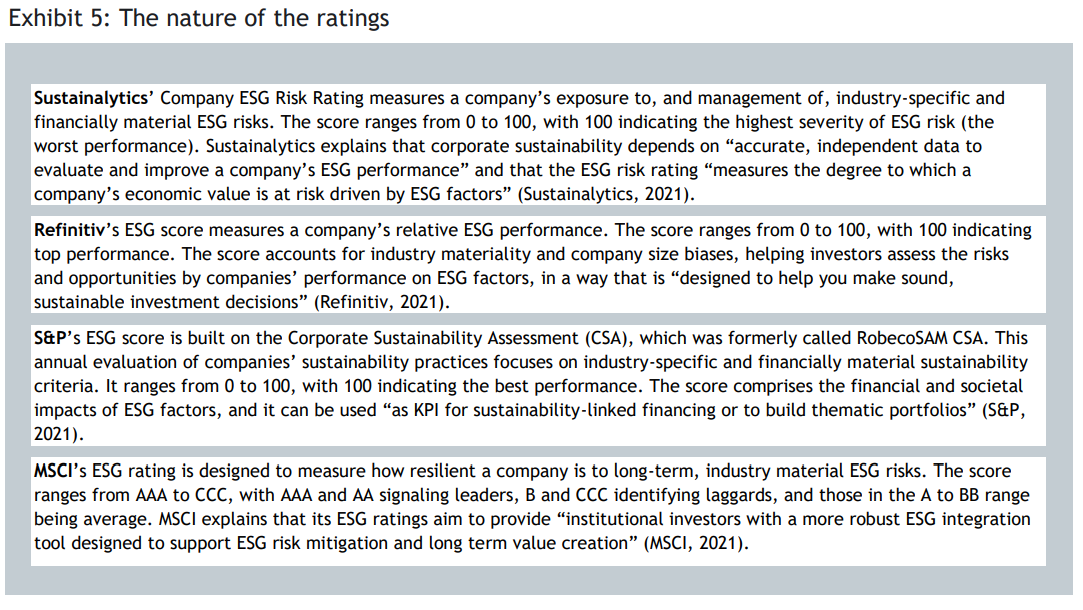

Exhibit 4 provides a summary of how major vendors source data inputs, while Exhibit 5 summarizes the nature of the ratings that these vendors assign.

How do vendors source data? ESG data may come directly from a company, from regulatory filings, or from news stories—as long as the vendor can assure that the source is reliable.

How do vendors measure data? First, they must establish what they are measuring with the data—perhaps, for example, a company’s degree of exposure to financially relevant risks, its level of disclosure, or is ability to address risks or opportunities. Then, the vendors must establish both the method of assessing the data (qualitative, sampled, time-weighted, level, trend, or rate of change) and how the information will be aggregated into factors—groups of data that share similar facets associated with a given area.

ESG ratings are also applied to investment funds—based on the companies owned. As such, vendors assign ratings at the company level first, particularly public corporations (vendors also have ESG rating methodologies for sovereign and quasi-governmental entities, albeit with altered criteria). Along with growing investor interest in “sustainable” funds, data providers have seen new opportunities in aggregating that information at the portfolio level. In most cases, portfolio ratings are simply a weighted average of the underlying securities, with the occasional bonus or penalty for manager intent. These product-level ratings aim to provide asset owners with a snapshot of ESG metrics for their investments.

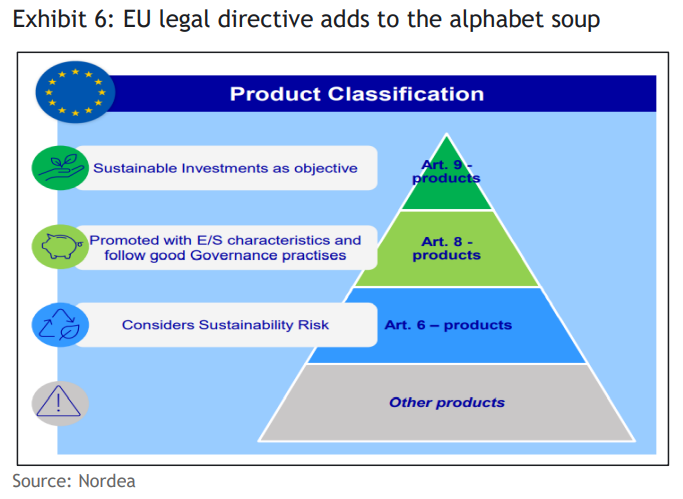

Measures of ESG risk and opportunity aren’t the only ESG “ratings” in the marketplace today. Adding confusion to the ESG-rating potpourri was the implementation of the European Sustainable Finance Disclosure Regulation (SFDR) in March 2021. The regulation was designed to make it easier for investors to distinguish and compare sustainable investment strategies available within the EU. SFDR aims to help investors by providing more transparency about the degree to which financial products consider environmental and/or social characteristics, invest in sustainable investments, or have sustainable objectives. The directive specifies three product classifications, as shown in Exhibit 6.

As well intentioned as the EU regulation was meant to be, the fund classifications have been used as another form of ESG “rating” (self-assigned by fund management organizations, no less) rather than as a disclosure standard for which the regulation was designed. The classifications assigned by SFDR were never meant to substitute investor due diligence in assessing a fund manager’s ESG and sustainability process, which is far more wide reaching and meaningful than just a disclosure standard. Further muddling things, regulators in the U.K. and U.S. are expected to release their own ESG fund classification schemes.

ESG ratings, notwithstanding their shortcomings, can still be of use to investors—albeit with appropriate caveats in terms of why, how, and when to use them. Ultimately, since there is no universal definition of what constitutes an ESG stock or fund, any use of ESG data or ratings comes down to an alignment of beliefs and expectations. In seeking such alignment, is there a more inclusive or comprehensive way for asset owners and financial intermediaries to assess the ESG credentials of their investments? We think SEI’s approach sheds some light toward that.

SEI’s approach

Underpinning SEI’s investment solutions is our well-established foundation of manager research and selection, which includes a proprietary ESG scoring system. Every firm and investment strategy that is subject to SEI’s comprehensive manager-research assessment undergoes an ESG due diligence review and receives a score of either Strong, Moderate, Limited, or Weak.

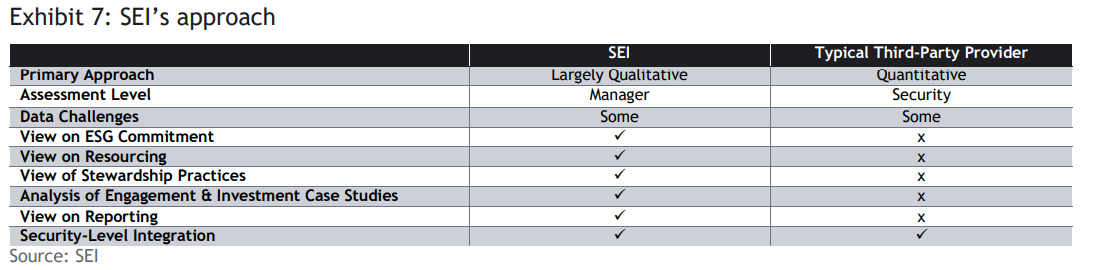

Unlike data vendors, our approach is more holistic and drives from the top-down (examining a manager’s espoused and evidenced actions) rather than the bottom-up (looking at holdings to infer a manager’s approach). Our ratings assess a firm’s cultural and organizational commitment to ESG and sustainable investing, from its ESG practices and policies as an entity to its allocation of resources to support the firm’s ESG commitment. At the individual investment strategy level, we get into the practical details of how ESG risks and opportunities are assessed and integrated into the investment decision-making process, their impact and influence on buy/sell/sizing of securities, and the level of activity and focus accorded to stewardship (the level and nature of a fund’s engagement with investee companies).

For the concerns noted above, we don’t rely much, if at all, on third-party ratings. This places the onus on qualitatively assessing commitment and action, resulting in detailed discussions with managers to evidence how they put ESG practices into action in both their investment and stewardship processes. We look for specific examples to support a manager’s words, and evaluate the quality of those examples. Manager transparency, therefore, is critical. Like any qualitative analysis, it is subjective. In order to minimize biases, we created criteria to define our qualitative assessment—providing transparency and consistency in guiding our final ratings, which are always subject to an analyst’s final judgment.

By combining firm and investment strategy ratings, we think our ratings provide a more comprehensive and complimentary picture of a manager’s ESG commitment and execution than a simple weighted average of security-level ratings. Exhibit 7 summarizes the key differences between SEI’s ratings approach and that of typical third-party vendors.

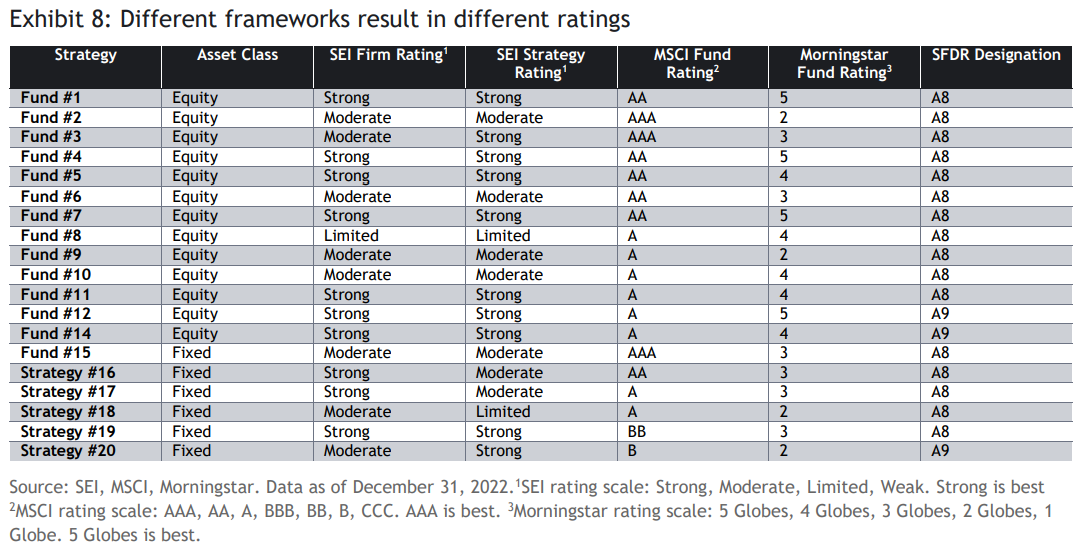

To put this into context, we looked at our ratings across a subset of managers that have MSCI and Morningstar ratings as well as SFDR designations. The data in Exhibit 8 details the various ratings these strategies carry (anonymized, as we don’t publish our ratings). While the majority of strategies achieved our minimum threshold of Moderate/Moderate (based on SEI on firm/strategy ratings) to be considered for an SEI-sponsored Article 8 fund, several of these strategies received “less-than-competitive” ratings from MSCI and/or Morningstar. This underscores, once again, the importance of investors paying close attention to how ratings were constructed, what drove the ratings, and how closely the ratings align with their own beliefs and ESG framework.

Disclosure and transparency matter

Media and investor focus on and questioning of ESG ratings isn’t about to go away any time soon. Perhaps some of the confusion will dissipate as more uniform collection and reporting standards come into effect (slowly), but what ESG and sustainable investing “means” to investors is not likely to be resolved with “better” ratings or a single score. While almost all investments are exposed to ESG risks and stewardship opportunities, how and what investors choose to do about that exposure will vary based on personal beliefs, objectives, and values. As such, when selecting sustainable investments, it remains critical to choose managers and strategies with well-articulated ESG philosophies and approaches, and can support their claims with evidenced decision-making.

To that end, disclosure and transparency are of paramount importance to investors as they provide the key to making informed decisions in the multi-dimensional and nuanced area of ESG ratings. At SEI, that openness (through our manager engagement program) has helped our clients and managers move forward with confidence on their journeys. We believe our transparency has fostered a greater understanding of our ratings methods—elevating trust among clients in our assessments and nurturing a deeper appreciation among managers of how we assess their ESG processes. To learn more or engage, please contact your SEI relationship manager.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

ESG and Sustainability are not uniformly defined across the industry. Environmental, social and governance (ESG) guidelines may cause a manager to make or avoid certain investment decisions when it may be disadvantageous to do so. This means that these investments may underperform other similar investments that do not consider ESG guidelines when making investment decisions. Sustainability is not uniformly defined and scores and ratings may vary across providers. Copyright© [2023] Sustainalytics. All rights reserved.

This communication contains information developed by Sustainalytics. Such information and data are proprietary of Sustainalytics and/or its third-party suppliers (Third Party Data) and are provided for informational purposes only. They do not constitute an endorsement of any product or project, nor an investment advice and are not warranted to be complete, timely, accurate or suitable for a particular purpose. Their use is subject to conditions available at https://www.sustainalytics.com/legal-disclaimers.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document, Summary of UCITS Shareholder rights (which includes a summary of the rights that shareholders of our funds have) and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents (https://seic.com/en-gb/fund-documents). And you should read the terms and conditions contained in the Prospectus (including the risk factors) before making any investment decision. If you are in any doubt about whether or how to invest, you should seek independent advice before making any decisions. Investments in SEI funds are generally medium to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may not get back the original amount invested.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to "institutional investors" pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to "relevant persons" pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the "SFO"). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorized and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI.

The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

For full details of all of the risks applicable to our funds, please refer to the SEI Funds prospectus on https://seic.com/en-gb/ourlocations/south-africa/fund-documents-south-africa.