Monthly Market Commentary: Equities Rise on Warming Trade Talks

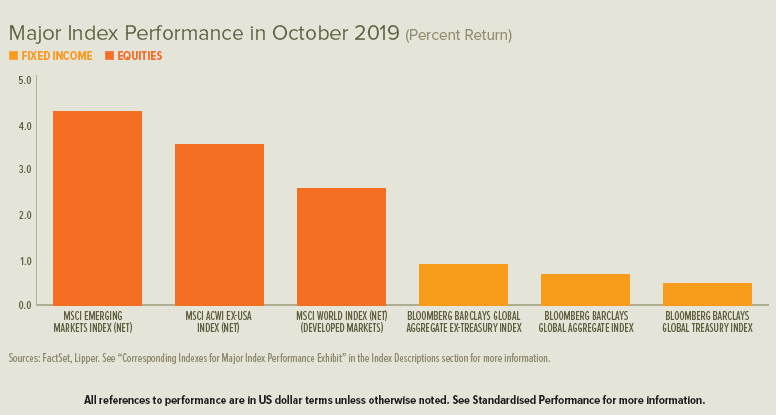

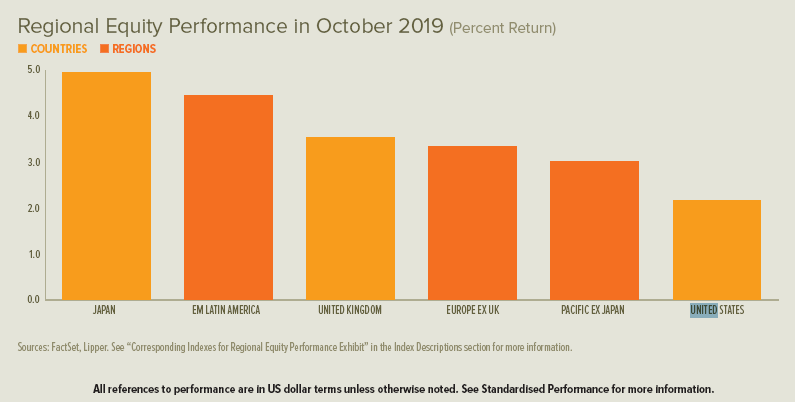

Global equity markets climbed at an accelerating pace in October with a boost from emerging markets. UK and European shares advanced sharply after a mediocre start to the month, while US and Japanese shares followed a steadier upward path. Mainland Chinese equity markets ended higher for the full month despite multiple rallies and selloffs; Hong Kong shares fared well after a soft start.

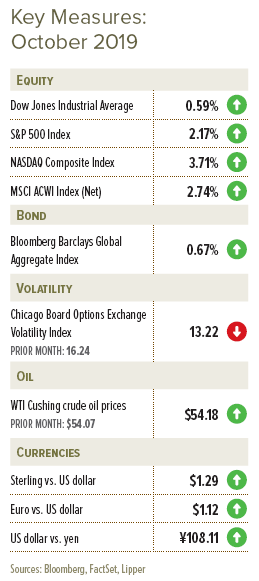

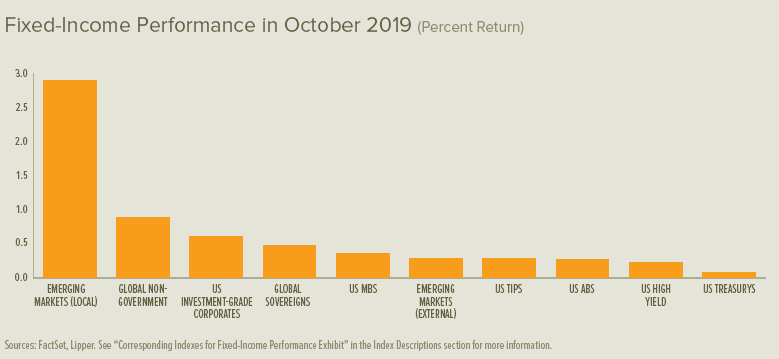

Government bond rates increased fairly evenly across all maturities in the UK and Europe during October, with long-term yields rising slightly more than short-term yields. In the US, short-term Treasury rates declined and long-term rates increased marginally. The opposing changes in US rates—driven largely by the US Federal Reserve’s most recent 0.25% cut to the federal-funds rate—resulted in the yield curve partially reverting to its “normal” upward slope, as longer-term Treasurys began to yield more than shorter-term Treasurys.

The UK’s unclear path out of the EU came into focus during October. Prime Minister Boris Johnson’s re-negotiated Brexit deal was deemed acceptable in principle by a majority of the House of Commons on 22 October—marking the furthest progress toward resolution up until that point—but was ultimately defeated in Parliament on concerns about executing the solution within its proposed three-day timetable. EU leaders agreed to extend the departure date again, this time from 31 October to the end of the calendar year. Jeremy Corbyn, the main opposition leader, consented to Johnson’s call for a snap election on 12 December, increasing the likelihood that a solid road to Brexit will be paved before the next departure date.

Trade relations appeared to thaw between the US and China—the two countries with the world’s largest economies, which together account for 40% of global gross domestic product (GDP)1. The US cancelled a planned 15 October increase in tariffs on Chinese products; later in the month, China announced $20 billion in purchases of US agricultural goods and declared willingness to soften policies on forced technology transfers and barriers to foreign investment.

Already-divisive US domestic politics turned sharply contentious as Democrats in the House of Representatives continued their impeachment inquiry into President Donald Trump—punctuating the month with a full House vote to formalise the investigation. Democrats began the probe in response to allegations that the US president urged Ukrainian President Volodymyr Zelensky to pursue investigations into Trump’s political opponents in exchange for $400 million of congressionally-approved military aid meant to counter a five-year Russian-backed insurgence in Eastern Ukraine. (The aid was eventually released in September once the allegations came into public view.) Toward the end of October, Zelensky—armed with the belatedly-released US military aid—succeeded in negotiating an artillery pullback from the front lines between Kremlin-backed separatist forces and the Ukrainian military.

Elsewhere in Eastern Europe, Polish and Hungarian voters continued to back the governing right-populist parties, but with less enthusiasm than in recent years: Poland’s Law and Justice party lost its majority in the Senate, while Hungary’s dominant Fidesz party lost mayoral races in a lengthy slate of major cities that included its capital city of Budapest.

Tensions rose in the Middle East after the US announced and then partially reversed a military withdrawal from Syria: Turkey and Russia exerted greater control in the country’s north, which put the US-allied Kurdish population at risk. The prime ministers of Iraq and Lebanon each announced their resignations in late October after weeks of growing anti-government protests rooted in economic dissatisfaction and concerns about corruption.

In South America, Chileans protesting higher subway fares remained in the streets despite producing concessions that included a pause on planned increases in electricity rates and a new slate of cabinet members. Brazil suffered one of the largest environmental disasters in its history during October when an oil spill off of its north-eastern shore (with no clear cause) spread to contaminate 2,200 kilometres of the country’s coastline.

Alberto Fernandez unseated Argentinian President Mauricio Macri after only one term in the country’s late-October election. While remarkable in that an Argentine incumbent lost for the first time, the result was unsurprising: Fernandez was expected to benefit from the popularity of his running mate, former President Cristina Fernandez de Kirchner. The prospect of a handover from conservatives to the centre-left Peronist movement during a period of crippling pressure on Argentina’s finances

raised anxiety among investors, particularly given the movement’s antagonistic relationship with foreign creditors. The International Monetary Fund (IMF) recently withheld $5 billion of loan aid in anticipation of the election results to determine whether Argentina’s leadership would maintain a commitment to austerity, which appeared unlikely given the Peronist platform.

Central Banks

- The Bank of England’s Monetary Policy Committee had no meeting in October.

- The European Central Bank (ECB) made no changes following October’s final monetary-policy meeting with Mario Draghi at its helm. The outgoing ECB president offered a defence of the central bank’s recent policy shift toward further accommodation, as Christine Lagarde, former managing director of the IMF, prepared to take the reins in November.

- The US Federal Open Market Committee announced an expected 0.25% decrease in the federal-funds rate toward the end of October, representing its third cut in as many meetings. In mid-October, the US central bank made its first monthly purchase of $60 billion in US Treasury bills as part of a programme to increase liquidity in the financial system.

- The Bank of Japan announced no change in its monetary policy programme following its late-October meeting.

Economic Data

- The contraction in UK manufacturing activity mostly levelled off during October, although new orders continued to slide as falling domestic demand overtook rising exports. Inventory stocking ahead of the 31 October Brexit deadline also contributed to the relative improvement in activity. The UK claimant count unemployment rate held firm at 3.3% during September, while the blended June-to-August UK unemployment rate edged up to 3.9%; average year-over-year earnings growth fell from 4.0% to 3.8%.

- Eurozone manufacturing continued to contract sharply in October, while modest services-sector growth eased slightly. Labour conditions in the eurozone were fair during September: The eurozone unemployment rate was unchanged at 7.5%—the lowest since July 2008—while the number of unemployed increased by 33,000 during the month. The eurozone economy continued to grow by 0.2% during the third quarter, while year-over-year growth slowed to 1.1% (from 1.2% in the second quarter).

- US manufacturing activity improved in October, contracting at a less significant pace, as export orders returned to growth territory. Services sector conditions continued to expand slowly. The US unemployment rate increased to 3.6% during the month despite a higher-than-expected gain in payrolls, an improved labour-force participation rate, and greater average hourly earnings.

SEI’s View

We have leaned toward an optimistic view on equities and other risk-oriented assets for the past 10 years. When markets corrected sharply in price—as several US equity indexes did in 2011, 2015 and late last year—we viewed the pullbacks as buying opportunities. We believe that staying invested has been a sound overall strategy. Today, while we still doubt that a true bear market is on the immediate horizon, we are surprised by the resilience of the stock-market averages during the third quarter in the face of numerous economic and political uncertainties, both in the US and globally.

The US economy remains in reasonably good shape and appears to be in little danger of contracting any time soon. Granted, the manufacturing and agricultural sectors are being stressed by the trade war with China. But we think there is a limit to how far this deterioration in economic activity will go. Few economists would dispute that the US consumer sector is in great shape.

Looking at the US stock market, the forward-earnings trend has flattened in recent quarters. Periods of flat-to-down earnings over several quarters occurred in the 2014-to-2015 period, and in 2011, 2007 and 1998, each coinciding with flat-to-declining stock prices, increased volatility and moderate-to-severe market corrections.

A trade truce between China and the US would be a relief, but it would be only one piece of a larger mosaic that must first come together. Getting the world back on a faster growth track will depend on an economic rebound in the domestic economies of China and Europe.

Our expectation of an economic revival in China rests on the assumption that all the fiscal and monetary-policy measures put in place over the past year will overcome the major challenge posed by the trade war. The latest tranches of import duties are aimed at Chinese goods like apparel and toys, which usually have thin profit margins, are labour-intensive, and can be more easily produced in other low-wage nations than higher-tech products. We therefore believe that Chinese President Xi Jinping has an incentive to get a deal done with President Trump. The last thing Xi needs is a sharp rise in unemployment and corporate bankruptcies as profit margins get eviscerated.

China’s currency has weakened further in recent months, remaining close to an 11-year low against the US dollar hit in September 2019 that amounted to a cumulative decline of 12% since April 2018—thereby offsetting a little more than half of the imposed or announced tariff increases. The Chinese government is reluctant to encourage additional currency depreciation, fearing that capital could flee the country. Rather, there is evidence that it is getting more aggressive when it comes to pulling the monetary and fiscal levers.

Slowing growth in China, the US and the eurozone does not bode well for other economies. On a positive note, many developing countries have been able to cut interest rates in recent months. Meanwhile, capital-market conditions in emerging countries still appear benign. Spreads on US dollar-denominated debt remain in the middle of their range for the past eight years.

Despite all its economic and political problems, European-wide equity markets have done rather well this year. How does one explain the rather robust performance of European equities? It can largely be attributed to the lack of an alternative option. For example, with Germany’s sovereign yield curve well into negative territory, its investors have no hope of building wealth in less risky fixed-income assets and are therefore forced into equities and other risk-oriented investments. Investors globally face similar challenges, even if not quite to the same extent.

While Germany’s overall economy is not clearly in a recession, its manufacturing sector almost certainly is—the 6.4% decline in industrial production from the peak in November 2017 through July 2019 was worse than Italy’s 2.5% contraction over the same period. Considering that manufacturing represents almost 23% of the country’s GDP (much higher than the average for developed countries), it is easy to understand why the country is struggling.

As we speculated last month, the UK was granted a new Brexit deadline. A general election scheduled for 12 December will hopefully produce a new mandate from the electorate. But the political landscape in Great Britain is in flux. The outcome of the next election could be an unstable coalition.

Despite the rather solid financial position of UK households, both consumer and business confidence are nearing levels consistent with recession. Confidence measures in the eurozone, while off the highs of 2017, have not fallen to the same degree.

Japan is also focused on home-grown uncertainty: The consumption tax hike effective 1 October. And despite a tight labour market with an almost record high number of available jobs per applicant, the decline in earnings growth from last year is surprisingly steep. Regardless of all their efforts, Prime Minister Shinzo Abe’s government and the Bank of Japan have been unable to spur a lasting reflation of the economy.

Like Germany, Japan has been hurt by the slowing growth of China and the general malaise affecting Asia as a whole. To make matters worse, Japan’s political relationship with South Korea has frayed badly in recent months. Both countries have expanded economic sanctions, including tit-for-tat tariff duties and consumer boycotts. Even more worrisome is the breakdown in direct military intelligence sharing at a time when China is pushing its weight around in the East and South China Seas.

In all, Japan’s outlook appears to be one of stasis. In the meantime, investors will likely continue to view the country as a safe haven owing to its low volatility. We believe the yen will remain well-bid under this scenario.

In view of the uncertainties facing investors presently, the prediction game is arguably even more challenging than usual. Accordingly, as always, we believe in a diversified approach to investing. Although maintaining exposure to equities and other risk-oriented assets can at times feel uncomfortable, it is our view that investors with long time horizons should avoid timing the market or making outsized sector or regional bets. We think it is best not to assume, for example, that the S&P 500 Index and growth stocks will always be the only games in town. The recent volatility and sharp style rotations in the past quarter should serve as reminders that trends do not last forever.

Glossary of Financial Terms

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.